Attorney-Approved Promissory Note Template for the State of Montana

Attorney-Approved Promissory Note Template for the State of Montana

In the state of Montana, individuals and entities often require a standardized method to formalize the act of lending money, ensuring that the borrower's promise to repay is legally documented. This need is fulfilled by the Montana Promissory Note form, a critical financial document that outlines the obligations of all parties involved. It specifies the amount of money loaned, the interest rate applied, and the repayment schedule agreed upon by the lender and borrower. Beyond these basics, the form also includes provisions for late fees and the consequences of non-payment, acting as a safeguard for the lender while providing a clear repayment roadmap for the borrower. The use of this form not only clarifies the terms of the financial agreement but also serves as a vital legal instrument should disputes arise, making it an indispensable tool in private financing within the state.

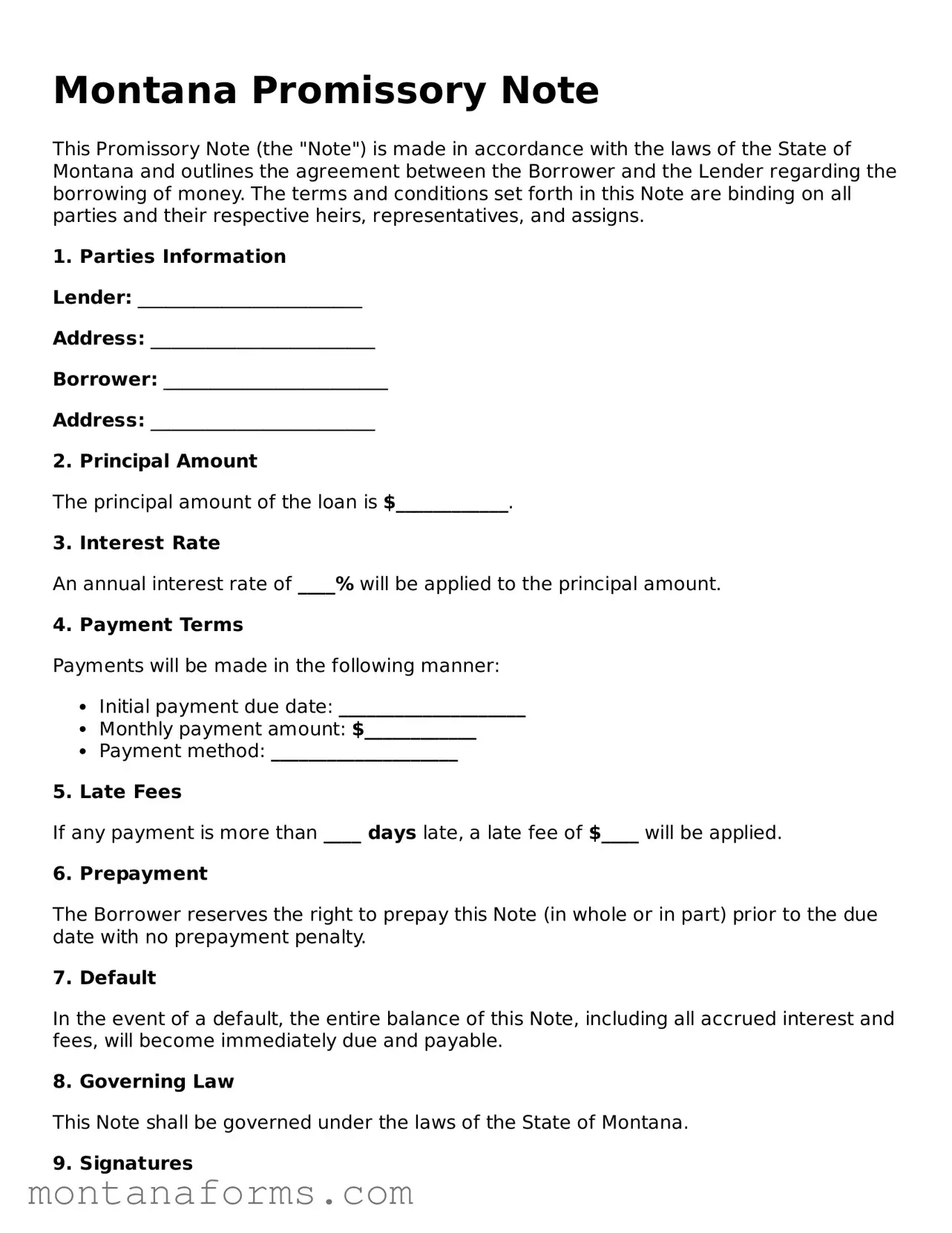

Montana Promissory Note

This Promissory Note (the "Note") is made in accordance with the laws of the State of Montana and outlines the agreement between the Borrower and the Lender regarding the borrowing of money. The terms and conditions set forth in this Note are binding on all parties and their respective heirs, representatives, and assigns.

1. Parties Information

Lender: ________________________

Address: ________________________

Borrower: ________________________

Address: ________________________

2. Principal Amount

The principal amount of the loan is $____________.

3. Interest Rate

An annual interest rate of ____% will be applied to the principal amount.

4. Payment Terms

Payments will be made in the following manner:

5. Late Fees

If any payment is more than ____ days late, a late fee of $____ will be applied.

6. Prepayment

The Borrower reserves the right to prepay this Note (in whole or in part) prior to the due date with no prepayment penalty.

7. Default

In the event of a default, the entire balance of this Note, including all accrued interest and fees, will become immediately due and payable.

8. Governing Law

This Note shall be governed under the laws of the State of Montana.

9. Signatures

By signing below, both parties agree to the terms and conditions of this Promissory Note.

_________________________

Lender's Signature

_________________________

Borrower's Signature

Date: _____________________

| Fact | Description |

|---|---|

| Governing Law | The Montana Promissory Note form is governed by Title 30, Chapter 3, Part 1 of the Montana Code Annotated (MCA), which aligns with the Uniform Commercial Code (UCC) as adopted in Montana. |

| Types | There are primarily two types of promissory notes in Montana: secured and unsecured. A secured note is backed by collateral, whereas an unsecured note is not, relying solely on the borrower's promise to pay. |

| Interest Rate | The legal interest rate in Montana is established by §31-1-106, MCA. The statutory limit without an agreement is 10% per annum. With a written agreement, parties may establish an interest rate not exceeding 15% per annum. |

| Usury Limit | If a loan exceeds the allowed interest rate, it is considered usurious, exposing the lender to potential fines and forfeiture of all interest on the debt, as prescribed by Montana usury laws in §31-1-107, MCA. |

| Signature Requirements | For a promissory note to be legally binding in Montana, it must be signed by the borrower and, in some cases, cosigners or guarantors to ensure the note's enforceability. |

| Prepayment | Borrowers in Montana are allowed to prepay their debts without facing a prepayment penalty, unless a prepayment penalty clause is explicitly stated in the promissory note agreement. |

| Release of Loan Commitment | Upon the fulfillment of the repayment terms, the lender is required to release the borrower from any further obligation by marking the promissory note as "paid in full" and returning it to the borrower. |

When completing a Montana Promissory Note form, it's essential to provide accurate and detailed information to ensure the agreement is legally binding and reflects the intentions of both the borrower and lender. A promissory note outlines the terms under which money is borrowed, including repayment schedule, interest rate, and the consequences of default. Following the correct steps to fill out the form reduces the risk of future disputes and ensures both parties understand their obligations.

By carefully completing each step, individuals can create a solid legal document that safeguards both the borrower's and lender's interests. It's always recommended to consult with a legal professional if there are any uncertainties during this process.

What is a Montana Promissory Note?

A Montana Promissory Note is a legal document that outlines a loan agreement between two parties - the borrower and the lender - within the state of Montana. It details the amount of money loaned, the interest rate applied, repayment schedule, and any other terms agreed upon by both parties. This document serves as a formal promise from the borrower to repay the borrowed sum under specified conditions, making it legally binding and enforceable in Montana courts.

Do I need to notarize my Montana Promissory Note?

While notarization is not a legal requirement for a promissory note to be considered valid in Montana, having your document notarized can add an extra layer of authenticity. Notarization is the process by which a public official (notary) verifies the identity of the parties signing the document, ensuring that signatures are genuine and that signers are not under duress. This can help prevent future disputes about the validity of the agreement.

What information should be included in a Montana Promissory Note?

What happens if the borrower fails to repay according to the terms of the Montana Promissory Note?

If the borrower fails to make payments as agreed in the Montana Promissory Note, they are considered to be in default of the loan. Depending on the terms outlined in the promissory note, the lender may have the right to demand immediate payment of the entire remaining balance of the loan (acceleration clause), initiate legal proceedings to collect the debt, and/or enforce any security interest if the loan was secured with collateral. It's crucial for borrowers to understand the consequences of not adhering to the repayment terms, as it could impact their financial stability and legal standing.

Filling out a promissory note in Montana is a crucial process, but it's easy to make mistakes that can have significant implications down the line. When people take the time to accurately complete this important document, they help protect their interests and ensure clarity regarding the terms of the agreement. Below are five common mistakes to avoid:

Not including all parties' full legal names: This might seem trivial, but the absence of the complete legal names can create confusion or legal disputes later on. The full names confirm who is obligated to repay the loan and who is owed the repayment.

Skipping the details of the loan: It’s crucial to spell out the loan amount, interest rate, repayment schedule, and due dates. Leaving out any of these details can result in misunderstandings and potential conflicts.

Forgetting to specify the interest rate: In Montana, if the promissory note doesn’t mention an interest rate, the loan might be subject to the state’s default interest rate. This oversight could lead to a lower return for the lender or legal issues.

Ignoring the default terms: Not stating what constitutes a default and the recourse actions available to the lender leaves too much to interpretation. Be clear about what happens if payments are late or missed.

Failing to get the document notarized: While not always a legal requirement, having the promissory note notarized adds a layer of authentication to the signatures and the agreement. This step can prove invaluable if the document’s validity is challenged.

By taking the time to carefully fill out the Montana Promissory Note form and avoiding these common pitfalls, both lenders and borrowers can safeguard their interests and ensure a smoother repayment process.

When preparing a Montana Promissory Note, several additional forms and documents are often utilized to ensure a comprehensive and legally binding agreement. These documents not only support the Promissory Note but also provide legal protections and clarify the responsibilities of all parties involved. Described below are six forms and documents commonly used alongside the Montana Promissory Note.

Together, these documents form a robust framework around the Montana Promissory Note, ensuring that all aspects of the loan are clearly defined and legally enforceable. By carefully preparing and including these additional forms and documents, lenders and borrowers can create a secure and transparent loan agreement that protects the interests of all parties involved.

The Montana Promissory Note form is akin to an IOU, which is an informal document acknowledging a debt. Both serve as agreements to pay back a specified sum of money to the lender by the borrower. However, the Promissory Note often contains more detailed information, including interest rates, repayment schedule, and the consequences of default, making it a more formal and binding document than a simple IOU.

Similar to a Loan Agreement, the Promissory Note outlines the terms under which money has been lent. They both detail the loan's amount, repayment terms, and interest rate. The key distinction is that Loan Agreements are typically more comprehensive, involving more clauses that cover legal ramifications in greater detail, and often involve a third party, such as a guarantor or collateral, as security for the loan. Promissory Notes tend to be simpler and imply a promise rather than creating a security interest.

The Mortgage Agreement shares similarities with the Promissory Note, as both concern the borrowing of money. The essential difference is that a Mortgage Agreement specifically ties the loan to a piece of real estate as collateral, ensuring the property can be foreclosed upon if the loan is not repaid. Conversely, a Promissory Note is not inherently secured by collateral but can be made secure if explicitly stated.

A Bill of Sale and a Promissory Note both function as proof of transactions. The former documents the sale and transfer of ownership of personal property (such as vehicles or equipment), while the latter acknowledges the borrowing of money and the commitment to repay it. Though their purposes differ, they both serve as legally binding documents that confirm and record an agreement between two parties.

Similar to a Promissory Note, a Personal Guarantee is associated with the borrowing of money. A Personal Guarantee is an agreement that someone other than the borrower—usually a business owner or executive—will repay a loan if the original borrower fails to do so. While a Promissary Note states the borrower’s promise to repay the lender directly, a Personal Guarantee adds an additional layer of security for the lender by holding another individual responsible.

The Deed of Trust is another document related to borrowing money, often used in real estate transactions. Like a Promissary Note, it involves an agreement to pay back a borrowed sum. However, a Deed of Trust involves three parties: the borrower, the lender, and a trustee. The borrower transfers the title of the real property to the trustee as security for the loan. Upon fulfillment of the Promissory Note’s conditions, the trustee reconveys the title to the borrower.

An Employment Agreement, though primarily about the terms of employment, shares a fundamental similarity with the Promissory Note in terms of being a binding agreement between two parties. Where an Employment Agreement outlines duties, compensation, and conditions of employment, a Promissory Note details the conditions under which one party promises to pay another. Both establish an obligation—one for providing services, the other for repaying a debt.

Student Loans, especially those documented through a Promissory Note, represent a special category. These notes detail the amount borrowed for education, the interest rate, and the repayment schedule. Unlike a typical Promissary Note, student loan notes are often more lenient in terms of repayment schedules, recognizing the borrower’s future income potential as a factor in loan repayment.

A Lease Agreement, while generally used to outline terms for renting property, bears resemblance to the Promissory Note in the commitment aspect. In a Lease, one party agrees to pay the other for the use of property for a specified term. Although it deals with property usage rather than lending money, the structure of a Lease—specifying terms, conditions, and the parties’ obligations—mirrors that of a Promissory Note’s approach to detailing a financial loan.

A Revolving Credit Agreement, like a Promissory Note, outlines a borrowing arrangement. Under a Revolving Credit Agreement, the borrower can repeatedly borrow up to a specified limit while repaying a portion of the debt over time. This flexibility in borrowing and repaying is distinct from the typically more fixed and straightforward borrowing structure of a Promissory Note, which usually details a singular loan and its repayment terms.

Filling out a Montana Promissory Note form requires careful attention to detail and an understanding of your obligations as the borrower or the terms you're setting as the lender. To ensure clarity and legality in this financial agreement, there are specific actions you should take, as well as avoid. Below are key dos and don'ts to consider:

Do:

Review Montana's state laws regarding promissory notes to ensure compliance, especially concerning interest rates and repayment terms.

Clearly outline the terms of the loan, including the principal amount, interest rate, repayment schedule, and any collateral involved, to prevent misunderstandings.

Include both the lender's and borrower's full legal names and addresses to accurately identify the parties involved in the agreement.

Sign the document in the presence of a notary public to validate the identity of the parties and enhance the enforceability of the note.

Don't:

Leave any sections blank, as incomplete information can lead to disputes or make the document unenforceable in court.

Ignore the requirement for witness signatures if specified under Montana law, as it could affect the document's legal standing.

Forget to provide each party with a copy of the signed promissory note for their records and future reference.

Fail to check the promissory note for errors or unclear terms before signing, as this document is legally binding and outlines the repayment obligations.

When it comes to the Montana Promissory Note form, there are several misconceptions that people may have. It's important to clear these up to ensure that when you're engaging in lending or borrowing, you fully understand the document you're using. Here's a closer look at these misunderstandies:

It’s the same as a loan agreement: Many people think a promissory note is the same as a loan agreement. While both documents are used for lending purposes, a promissory note is simpler. It includes the promise to pay, whereas a loan agreement provides more detailed terms and conditions of the loan.

It doesn’t need to be signed: A common misconception is that a promissory note doesn’t need to be signed to be valid. In truth, for the promissory note to be legally binding in Montana, it must be signed by the borrower and, in some cases, the lender as well.

Verbal agreements are just as good: Some believe that verbal agreements can serve the same purpose as a written promissory note. However, a written and signed promissory note is far stronger in a court of law should any dispute arise regarding the loan.

It only needs to include the amount borrowed: While the amount borrowed is a critical component of the promissory note, it is a misconception that it's the only thing that needs to be included. In reality, the note should also contain payment terms, interest rates, and what happens in the case of a default, among others, to be fully effective and clear.

Understanding these key points can help both lenders and borrowers navigate their financial transactions more effectively and avoid potential legal issues that could arise from misunderstandings about the Montana Promissory Note form.

When considering the use of a Montana Promissory Note form, it's essential to understand its purpose and the implications of filling it out and using it correctly. This document is a legal agreement that outlines the terms under which money is borrowed and repaid. The following key takeaways can help guide you through the process:

In summary, when filling out and using the Montana Promissory Note form, attention to detail and clarity in documenting the terms of the loan are paramount. The form is a critical component of ensuring both parties understand their rights and obligations, and it can serve as a valuable point of reference in the event of a dispute. By following these key takeaways, borrowers and lenders can navigate the process more confidently and securely.

Montana Buy Sell Agreement - It must be signed by both parties to be enforceable, making it a critical step in the property buying process.

How to Make an Operating Agreement - This agreement sets the guidelines for how the business will run, including member duties and financial decisions.