Fillable Montana W 9 Template in PDF

Fillable Montana W 9 Template in PDF

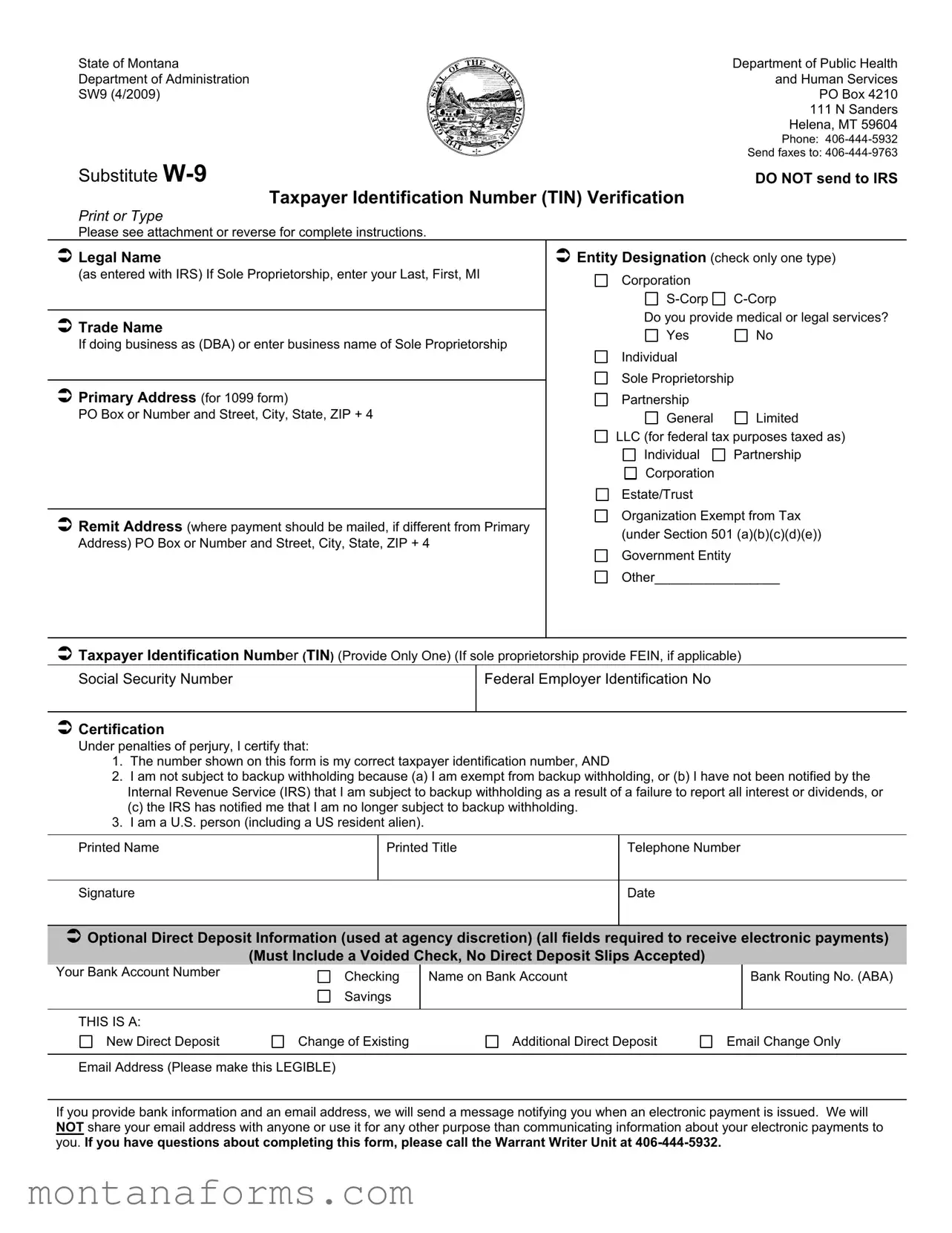

In Montana, professionals and businesses engaging with state departments must familiarize themselves with the Substitute W-9 Taxpayer Identification Number (TIN) Verification form. This form, a cornerstone for transactions involving the State of Montana Department of Public Health, Department of Administration, and Human Services, serves a pivotal role in streamlining the identification process for tax purposes. Its importance cannot be overstated, as it directly impacts the efficiency of processing payments and ensuring compliance with tax laws. The form requires detailed information such as the legal name, entity designation, primary and remit addresses, and the taxpayer's correct TIN, which could either be a Social Security Number or a Federal Employer Identification Number, depending on the entity's nature. Additionally, the form includes a certification section where the taxpayer attests to the accuracy of the provided information and their exemption status from backup withholding, under the penalties of perjury. This process not only aids in accurate tax reporting but also safeguards taxpayers from potential issues related to backup withholding and incorrect TIN reporting, which could result in delayed payments or penalties. Moreover, the form facilitates the option for direct deposit, promising a smoother transaction experience for vendors and service providers. By adhering to the instructions and correctly filling out the form, entities ensure their compliance and contribute to a more efficient state administration system.

State of Montana |

Department of Public Health |

Department of Administration |

and Human Services |

SW9 (4/2009) |

PO Box 4210 |

|

111 N Sanders |

|

Helena, MT 59604 |

|

Phone: |

|

Send faxes to: |

Substitute

Taxpayer Identification Number (TIN) Verification

DO NOT send to IRS

Print or Type

Please see attachment or reverse for complete instructions.

Legal Name |

Entity Designation (check only one type) |

||

(as entered with IRS) If Sole Proprietorship, enter your Last, First, MI |

Corporation |

|

|

|

|

||

|

|||

|

Do you provide medical or legal services? |

||

Trade Name |

|||

Yes |

No |

||

If doing business as (DBA) or enter business name of Sole Proprietorship |

|||

Individual |

|

||

|

|

||

|

Sole Proprietorship |

||

Primary Address (for 1099 form) |

|||

Partnership |

|

||

PO Box or Number and Street, City, State, ZIP + 4 |

General |

Limited |

|

|

|||

|

LLC (for federal tax purposes taxed as) |

||

|

Individual |

Partnership |

|

|

Corporation |

|

|

|

Estate/Trust |

|

|

|

Organization Exempt from Tax |

||

Remit Address (where payment should be mailed, if different from Primary |

|||

(under Section 501 (a)(b)(c)(d)(e)) |

|||

Address) PO Box or Number and Street, City, State, ZIP + 4 |

|||

Government Entity |

|

||

|

|

||

|

Other_________________ |

||

|

|

|

|

Taxpayer Identification Number (TIN) (Provide Only One) (If sole proprietorship provide FEIN, if applicable)

Social Security Number

Federal Employer Identification No

Certification

Under penalties of perjury, I certify that:

1.The number shown on this form is my correct taxpayer identification number, AND

2.I am not subject to backup withholding because (a) I am exempt from backup withholding, or (b) I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or

(c)the IRS has notified me that I am no longer subject to backup withholding.

3.I am a U.S. person (including a US resident alien).

Printed Name

Printed Title

Telephone Number

Signature

Date

Optional Direct Deposit Information (used at agency discretion) (all fields required to receive electronic payments) (Must Include a Voided Check, No Direct Deposit Slips Accepted)

Your Bank Account Number |

Checking |

Name on Bank Account |

Bank Routing No. (ABA) |

|

|||

|

Savings |

|

|

|

|

|

|

THIS IS A: |

|

|

|

New Direct Deposit

Change of Existing

Additional Direct Deposit

Email Change Only

Email Address (Please make this LEGIBLE)

If you provide bank information and an email address, we will send a message notifying you when an electronic payment is issued. We will NOT share your email address with anyone or use it for any other purpose than communicating information about your electronic payments to

you. If you have questions about completing this form, please call the Warrant Writer Unit at

SW9 (4/2009)

Instructions for Completing Taxpayer Identification Number Verification

(Substitute

Legal Name As entered with IRS

Individuals: Enter Last Name, First Name, MI

Sole Proprietorships: Enter Last Name, First Name, MI

LLC Single Owner: Enter owner's Last Name, First Name, MI

All Others: Enter Legal Name of Business

Trade Name

Individuals: Leave Blank

Sole Proprietorships: Enter Business Name

LLC Single Owner: Enter LLC Business Name

All Others: Complete only if doing business as a D/B/A

Primary Address

Address where 1099 should be mailed.

Remit Address

Address where payment should be mailed. Complete only if different from primary address.

Entity Designation

Check ONE box which describes the type of business entity.

Taxpayer Identification Number

LIST ONLY ONE: Social Security Number OR Employer Identification Number. See “What Name and Number to Give the Requester” at right.

If you do not have a TIN, apply for one immediately. Individuals use federal form

Certification

You must cross out item 2 above if you have been notified by the IRS that you are currently subject to backup withholding because you have failed to report all interest and dividends on your tax return. For real estate transactions, item 2 does not apply. For mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirement arrangement (IRA), and generally, payments other than interest and dividends, you are not required to sign the certification, but you must provide your correct TIN.

Privacy Act Notice

Section 6109 of the Internal Revenue Code requires you to furnish your correct TIN to persons who must file information returns with the IRS to report interest, dividends, and certain other income paid to you, mortgage interest you paid, the acquisition or abandonment of secured property, or contributions you made to an IRA. The IRS uses the numbers for identification purposes and to help verify the accuracy of your tax return. You must provide your TIN whether or not you are required to file a tax return. Payers must generally withhold 28% of taxable interest, dividend, and

certain other payments to a payee who does not furnish a TIN to a payer. Certain penalties may also apply.

What Name and Number to Give the Requester

For this type of account: |

Give name and SSN of: |

||

1. |

Individual |

The individual |

|

2. |

Two or more individuals (joint |

The actual owner of the account |

|

|

account) |

or, if combined funds, the first |

|

|

|

individual no the account 1 |

|

3. |

Custodian account of a minor |

The minor 2 |

|

|

(Uniform Gift to Minors Act) |

|

|

4. a. The usual revocable savings |

The |

||

|

trust (grantor is also trustee) |

|

|

|

b. |

The actual owner 1 |

|

|

is not a legal or valid trust |

|

|

|

under state law |

|

|

5. |

Sole proprietorship or Single- |

The owner |

3 |

|

Owner LLC |

|

|

|

|

|

|

For this type of account: |

Give name and EIN of: |

||

6. |

Sole Proprietorship or Single- |

The owner 3 |

|

|

Owner LLC |

|

|

7. |

A valid trust, estate, or pension |

Legal entity 4 |

|

|

trust |

|

|

8. |

Corporate or LLC electing |

The corporation |

|

|

corporate status on Form |

|

|

|

8832 |

|

|

9. |

Association, club, religious, |

The organization |

|

|

charitable, educational, or |

|

|

|

other |

|

|

10. Partnership or |

The partnership |

||

|

LLC |

|

|

11. A broker or registered |

The broker or nominee |

||

|

nominee |

|

|

12. Account with the Department |

The public entity |

||

|

of Agriculture in the name of a |

|

|

|

public entity (such as a state |

|

|

|

or local government, school |

|

|

|

district or prison) that receives |

|

|

|

agricultural program payments |

|

|

|

|

|

|

1List first and circle the name of the person whose number you furnish. If only one person on a joint account has an SSN, that person’s number must be furnished.

2 Circle the minor’s name and furnish the minor’s SSN.

3 You must show your individual name, but you may also enter your business or “DBA” name. You may use either your SSN or EIN (if you have one).

4 List first and circle the name of the legal trust, estate, or pension trust. (Do not furnish the TIN of the personal representative or trustee unless the legal entity itself is not designated in the account title.)

NOTE: If no name is circled when more than one name is listed, the number will be considered to be that of the first name listed.

Taxpayer Identification Request

In order for the State of Montana to comply with the Internal Revenue Service regulations, this letter is to request that you complete the enclosed Substitute Form

Please return or FAX the Substitute Form

We are required to inform you that failure to provide the correct Taxpayer Identification Number (TIN) / Name combination may subject you to a $50 penalty assessed by the Internal Revenue Service under Section 6723 of the Internal Revenue Code.

Only the individual’s name to which the Social Security Number was assigned should be entered on the first line.

The name of a partnership, corporation, club, or other entity, must be entered on the first line exactly as it was registered with the IRS when the Employer Identification Number was assigned.

DO NOT submit your name with a Tax Identification Number that was not assigned to your name. For example, a doctor MUST NOTsubmit his or her name with the Tax Identification Number of a clinic he or she is associated with.

Thank you for your cooperation in providing us with this information. Please return the completed form to Department of Public Health and Human Services, Business and Financial Services Division:

DPHHS, BFSD

PO Box 4210

Helena, MT 59604

Phone:

Fax:

| Fact | Detail |

|---|---|

| Form Title | Substitute W-9 Taxpayer Identification Number (TIN) Verification |

| Issuing Body | State of Montana Department of Public Health and Human Services, Department of Administration |

| Form Version | SW9 (4/2009) |

| Purpose | To verify the taxpayer identification number (TIN) for the State of Montana's vendor files. |

| Primary Use | Ensuring compliance with IRS regulations and updating the State's vendor file with the most current information. |

| Who Must File | Individuals and entities providing services or receiving payments from the State of Montana that require reporting to the IRS. |

| Penalty for Non-Compliance | Delayed payments or backup withholding, and potentially a $50 penalty assessed by the IRS under Section 6723 of the Internal Revenue Code for failure to provide the correct name/TIN combination. |

| Contact Information | Phone: 406-444-5932, Fax: 406-444-9763 |

The Montana W-9 form is essential for the State of Montana to accurately report income and comply with IRS regulations. This form requests your Taxpayer Identification Number (TIN), which is crucial for processing payments and avoiding potential backup withholding. To ensure timely payment and compliance, carefully follow these steps to complete the form correctly.

After completing the form, return it to the Department of Public Health and Human Services, Business and Financial Services Division at the provided address or fax number. Timely submission of this form ensures that your payments are processed without unnecessary delays or withholdings. Keep a copy of the completed form for your records.

What is the Montana W-9 form used for?

The Montana W-9 form is a document designed to provide a taxpayer's identification number (TIN), which can be either a Social Security Number (SSN) or an Employer Identification Number (EIN), to entities that pay income to the person completing the form. This is necessary for the State of Montana, particularly the Department of Public Health and Human Services and the Department of Administration, to comply with Internal Revenue Service (IRS) regulations. It's used for verification purposes to ensure the accuracy of information returns filed with the IRS, such as reporting interest, dividends, and other payments. Importantly, it helps in updating the State's vendor file with current information, which is essential for processing payments accurately and efficiently.

Who needs to complete the Montana W-9 form?

Individuals, businesses, and other entities that receive payments from the State of Montana for providing goods and services are required to complete the Montana W-9 form. This includes sole proprietors, corporations, partnerships, and exempt organizations among others. If you are a vendor to the State or involved in any transaction where the State has to report the payments to the IRS, you should fill out this form. Additionally, anyone who is directed by the Montana Department of Administration, State Accounting Division, to provide their Taxpayer Identification Number must also fill out this form to avoid delayed payments or backup withholding.

What are the consequences of not submitting the Montana W-9 form?

If the Montana W-9 form is not submitted, or if it's submitted incomplete or incorrect, there are several potential consequences. The primary consequence is delayed payments. The State might hold payments until they receive a properly completed form. Moreover, failure to provide this information within the given timeframe, which is usually (10) days from the receipt of the request, could result in the State of Montana applying a 28% withholding on each payment made to the entity. Additionally, not providing a correct TIN/Name combination may subject the provider to a $50 penalty imposed by the IRS under Section 6723 of the Internal Revenue Code. It's crucial for vendors and other payees to provide accurate information promptly to avoid these issues.

How can I submit the completed Montana W-9 form?

To submit the completed Montana W-9 form, individuals and entities can either mail it or send it via fax to the Department of Public Health and Human Services, Business and Financial Services Division. The mailing address is DPHHS, BFSD, PO Box 4210, Helena, MT 59604. If preferring to fax the form, the fax number is 406-444-9763. It's essential to ensure that the form is filled out completely and correctly before submission to avoid delays in processing or potential withholding. Additionally, the form asks for optional direct deposit information—if this method is preferred, make sure to include a voided check (not a deposit slip) with your submission.

When filling out the Montana W-9 form, individuals commonly make several mistakes, leading to processing delays or incorrect tax documentation. Identifying these errors can ensure smoother interactions with the State of Montana Department of Public Health and Human Services. Below are four such mistakes individuals frequently make:

In summary, accurately completing the Montana W-9 form involves careful attention to the details provided regarding one's tax identification and entity status. Ensuring that all information is correct and corresponds with IRS records is critical to avoid the common mistakes listed above.

In the realm of business administration and financial compliance, the Montana W-9 form is a cornerstone document for entities and individuals engaged in professional transactions that necessitate reporting and verification of taxpayer identification numbers (TINs). However, to ensure thorough compliance and smooth financial operations, several additional forms and documents are often used concurrently with the Montana W-9 form. Each of these documents serves a specific purpose, contributing to a comprehensive compliance framework.

Understanding the purpose and requirements of these forms can significantly enhance the accuracy of financial reporting and compliance efforts. While some forms, like the W-4 and 1099-MISC, directly relate to employee and contractor payments, others, such as the Form 8832 or SS-4, are foundational for the entity's legal and tax structure. Together with the Montana W-9 form, these documents help establish a robust framework for financial and tax compliance, ensuring that entities can navigate the complexities of reporting obligations with confidence.

The Montana W-9 form is closely related to the Federal W-9 Form, with its primary role being to provide a taxpayer identification number and certification for entities or individuals that engage in financial transactions that necessitate tax reporting. Both forms serve as a way to gather necessary information from vendors, contractors, or freelancers, ensuring that appropriate tax documentation can be generated, particularly the 1099 forms for independent contractors. By collecting details such as legal name, trade name, Taxpayer Identification Number (TIN), and entity type, they streamline tax reporting and compliance with IRS regulations.

IRS Form W-4, the Employee's Withholding Certificate, shares similarities with the Montana W-9 in terms of collecting taxpayer information. However, the W-4’s function is primarily for employers to determine the correct amount of federal income tax to withhold from employees' paychecks. While the W-9 is used to verify the taxpayer identification number and the individual’s status concerning backup withholding, the W-4 collects personal allowance information to adjust the tax withholding rate.

The Form 1099-MISC mirrors the Montana W-9’s goal of facilitating accurate tax reporting. The information provided on a W-9 allows payers to properly complete Form 1099-MISC, which reports non-employee compensation. The link between these documents is crucial; the payer uses the TIN or SSN provided on the W-9 to report the payments made to the IRS and the payee on the 1099-MISC, highlighting a direct connection in the tax reporting procedure for non-employee compensation.

Similar in purpose to the Montana W-9 is the Form W-8BEN, "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)." While W-9 forms are used by U.S. persons, the W-8BEN is completed by non-U.S. persons to certify their foreign status and claim any applicable treaty benefits, including a reduced rate of, or exemption from, withholding as part of their financial activities within the U.S. Both forms help in asserting the payee’s tax status, but each applies to residents of different jurisdictions.

The relationship between the Montana W-9 and the Form 1099-INT is established through the requirement of taxpayer information for accurate interest income reporting. Banks and financial institutions use the details provided on a W-9, such as the individual or entity's TIN, to issue a 1099-INT form correctly. This form reports interest income to the IRS, connecting the requirement for accurate identification information with the duty of reporting certain types of income.

The State Resale Certificate shares a procedural similarity with the Montana W-9, as both are used in transactions to verify a party’s information for tax purposes. Resale certificates are used by businesses to purchase goods intended for resale without paying sales tax at the point of purchase. The transparency and accountability in tax-related information, as seen with the TIN verification on a W-9, are central to both documents, albeit serving different ends in tax responsibility and compliance.

Form 1040, the U.S. Individual Income Tax Return, although more comprehensive, connects with the Montana W-9 through the necessity of reporting accurate taxpayer identification. The information provided on a W-9 may affect the reporting and taxation of income that individuals must disclose on their Form 1040. Which income is subject to report and tax might be partly determined based on documentation like the 1099 forms, which rely on the information provided by the W-9.

Akin to the W-9's function in business and tax documentation, the Form SS-4, Application for Employer Identification Number (EIN), is another vital link in the tax reporting chain. Businesses often need an EIN for tax purposes, which is used in various business activities and reporting obligations. The details an entity provides on a W-9, including its EIN, play a direct role in ensuring that transactions are properly reported to the IRS, underlining their connection in business identification and tax compliance.

The Form 8822, Change of Address, aligns with the W-9 in ensuring that the IRS has up-to-date information. While the primary role of the W-9 is to verify TINs, keeping current addresses is crucial for correct document delivery, such as tax return filings and correspondences. The necessity for updated information for tax compliance and communication purposes links these forms in administrative functionality.

Lastly, the Form 8832, Entity Classification Election, relates to the Montana W-9 by detailing the tax classification of entities. An LLC, for example, might use Form 8832 to elect its tax treatment (as a corporation, partnership, or disregarded entity), which then informs how it should be treated on the W-9. Understanding the entity’s classification helps in correctly completing the W-9 and ensuring that tax reporting and liability reflect the entity’s current status.

When completing the Montana Substitute W-9 Form, certain procedures should be followed to ensure the accuracy and compliance of the information provided. This guidance outlines the dos and don'ts of this process.

Do:

Don't:

Following these guidelines closely will help ensure your Substitute W-9 form for Montana is filled out accurately and in compliance, facilitating proper payment and reporting procedures.

There are several misconceptions about the Montana W-9 form and its requirements. Understanding these misconceptions can help ensure accurate completion and submission of the form.

Clearing up these misconceptions ensures that the Montana W-9 form is filled out correctly and that individuals and entities comply with state guidelines, avoiding delays or penalties.

It's crucial to provide accurate information on the Montana W-9 Form to avoid delayed payments and potential penalties. Understand the importance of correctly filling out and using this form with the following key takeaways.

Timely and accurate completion and submission of the Montana W-9 form are essential. It not only ensures compliance with tax regulations but also facilitates a smoother payment process for businesses and individuals engaged with the State of Montana.

What Wages Are Subject to Illinois Unemployment Tax - Historical wage data is necessary for assessing the current unemployment insurance contribution.

Montana Homesteading - A legal instrument by which Montana residents can claim homestead protections, affording their home certain immunities from forced sales.