Fillable Montana Pr 1 Template in PDF

Fillable Montana Pr 1 Template in PDF

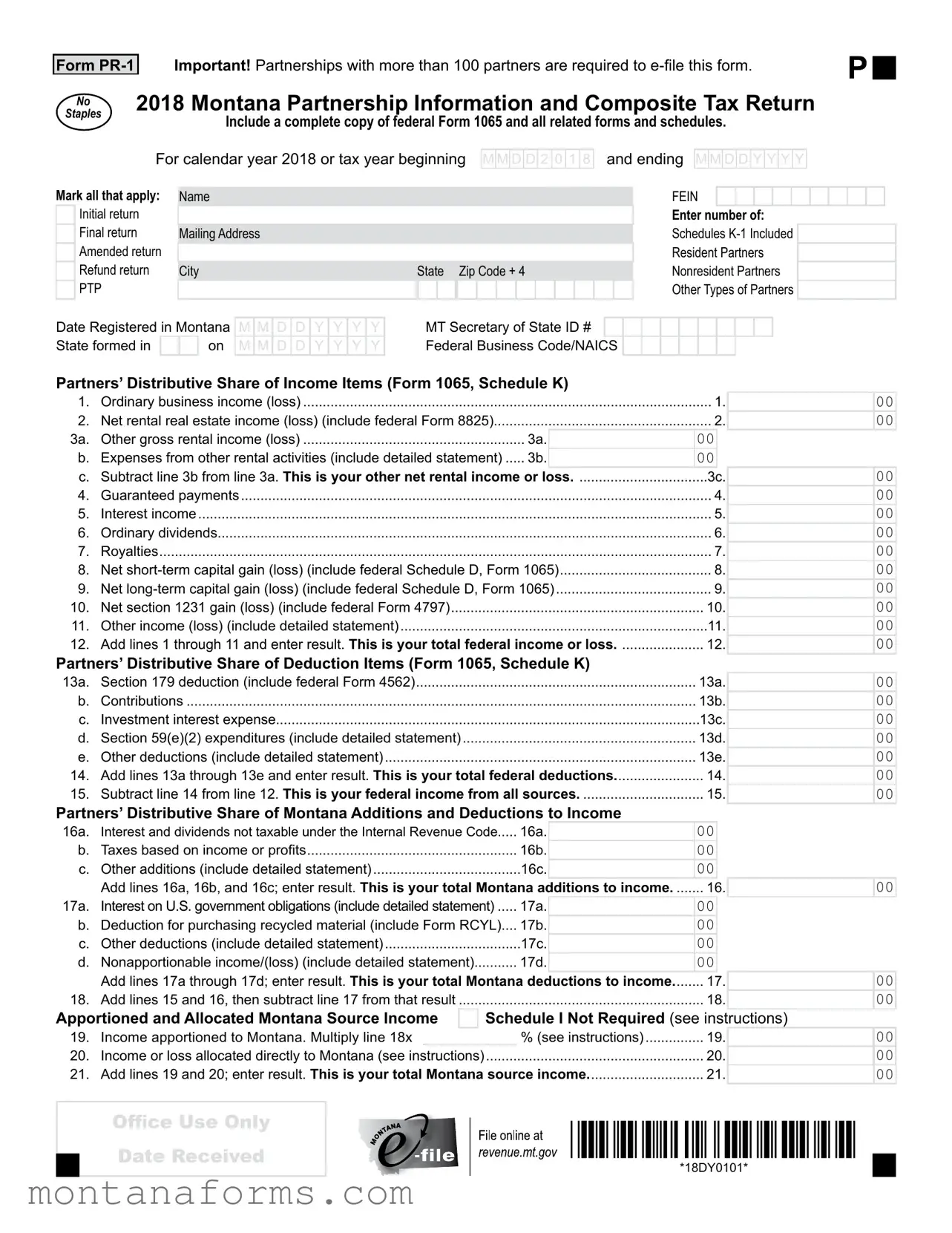

Navigating the complexities of partnership taxation in Montana requires familiarity with specific forms, one of which is the Montana PR-1 form. Notably designed for partnerships that number their partners above 100, the mandate to e-file brings convenience and efficiency to the process. The essential purpose of the document is for compiling partnership information and composite tax returns, which includes a comprehensive cross-section of financial activities such as ordinary business gains or losses, dividends, and interests among others. Crucially, it demands a detailed recitation of federal income and deductions, as well as specific adjustments pertinent to Montana's tax regulations. Additionally, the form plays a critical role in apportioning income to Montana for multi-state partnerships and calculating the overall tax liability or refunds due. The inclusion of detailed schedules, such as Schedule K-1 for partners and various tax credits, highlights the state's approach to ensuring fair and accurate taxation while providing avenues for tax relief. As with many tax documents, accuracy and thoroughness in completing the form are paramount, underscoring the pivotal role it plays in the broader landscape of partnership taxation within the state.

Form |

Important! Partnerships with more than 100 partners are required to |

P |

|

No |

2018 Montana Partnership Information and Composite Tax Return |

|

|

|

|

|

|

Staples |

Include a complete copy of federal Form 1065 and all related forms and schedules. |

|

|

|

|

|

For calendar year 2018 or tax year beginning

M M

M D

D D

D 2 0

2 0  1 8

1 8

and ending

M M D D

D D Y

Y Y

Y Y

Y Y

Y

Mark all that apply:

Initial return Final return Amended return Refund return

PTP

Name

Mailing Address

City |

State Zip Code + 4 |

FEIN

Enter number of:

Schedules

Resident Partners

Nonresident Partners

Other Types of Partners

Date Registered in Montana |

M |

M |

D |

D |

Y |

Y |

Y |

Y |

MT Secretary of State ID # |

|

|

|

|

|

|

|

|

|

|||

State formed in |

|

|

on |

M |

M |

D |

D |

Y |

Y |

Y |

Y |

Federal Business Code/NAICS |

|

|

|

|

|

|

|

|

|

Partners’ Distributive Share of Income Items (Form 1065, Schedule K) |

|

|||

1. |

Ordinary business income (loss) |

|

1. |

|

2. |

Net rental real estate income (loss) (include federal Form 8825) |

2. |

||

3a. |

Other gross rental income (loss) |

3a. |

00 |

|

b. |

Expenses from other rental activities (include detailed statement) |

3b. |

00 |

|

c. |

Subtract line 3b from line 3a. This is your other net rental income or loss |

3c. |

||

4. |

Guaranteed payments |

|

4. |

|

5. |

Interest income |

|

5. |

|

6. |

Ordinary dividends |

|

6. |

|

7. |

Royalties |

|

7. |

|

8. |

Net |

8. |

||

9. |

Net |

9. |

||

10. |

Net section 1231 gain (loss) (include federal Form 4797) |

|

10. |

|

11. |

Other income (loss) (include detailed statement) |

|

11. |

|

12. |

Add lines 1 through 11 and enter result. This is your total federal income or loss |

12. |

||

Partners’ Distributive Share of Deduction Items (Form 1065, Schedule K) |

|

|||

13a. |

Section 179 deduction (include federal Form 4562) |

|

13a. |

|

b. |

Contributions |

|

13b. |

|

c. |

Investment interest expense |

|

13c. |

|

d. |

Section 59(e)(2) expenditures (include detailed statement) |

|

13d. |

|

e. |

Other deductions (include detailed statement) |

|

13e. |

|

14. |

Add lines 13a through 13e and enter result. This is your total federal deductions |

14. |

||

15. |

Subtract line 14 from line 12. This is your federal income from all sources |

15. |

||

Partners’ Distributive Share of Montana Additions and Deductions to Income |

|

|||

16a. |

Interest and dividends not taxable under the Internal Revenue Code |

16a. |

00 |

|

b. |

Taxes based on income or profits |

16b. |

00 |

|

c. |

Other additions (include detailed statement) |

16c. |

00 |

|

|

Add lines 16a, 16b, and 16c; enter result. This is your total Montana additions to income |

16. |

||

17a. |

Interest on U.S. government obligations (include detailed statement) |

17a. |

00 |

|

b. |

Deduction for purchasing recycled material (include Form RCYL).... |

17b. |

00 |

|

c. |

Other deductions (include detailed statement) |

17c. |

00 |

|

d. |

Nonapportionable income/(loss) (include detailed statement) |

17d. |

00 |

|

|

Add lines 17a through 17d; enter result. This is your total Montana deductions to income |

17. |

||

18. |

Add lines 15 and 16, then subtract line 17 from that result |

|

18. |

|

Apportioned and Allocated Montana Source Income |

Schedule I Not Required (see instructions) |

|||

19. |

Income apportioned to Montana. Multiply line 18x |

|

% (see instructions) |

19. |

20. |

Income or loss allocated directly to Montana (see instructions) |

........................................................ |

20. |

|

21. |

Add lines 19 and 20; enter result. This is your total Montana source income |

21. |

||

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Office Use Only Date Received

*18DY0101*

*18DY0101*

*18DY0101*

Form |

FEIN |

|

|

Calculation of Amount Owed or Refund |

|

|

|

22. |

Enter your Montana total composite tax from Schedule IV, column H |

............................................... |

22. |

23. |

Enter the sum of |

23. |

|

Withholding |

|

|

|

24 a. Total Montana mineral royalty tax withheld on your behalf (see instructions) 24a. |

00 |

||

|

b. Mineral royalty tax withheld distributed to partners |

24b. |

00 |

|

c. Subtract 24b from 24a. Montana mineral royalty tax withheld attributable to partnership |

24c. |

|

25 a. Total Montana |

00 |

||

|

b. Montana |

25b. |

00 |

|

c. Subtract line 25b from 25a. Montana |

25c. |

|

26. |

Add lines 24c and 25c. This is the total withholding payments attributable to partnership |

26. |

|

Return Payments

00

00

00

00

00

00

27 a. |

2017 overpayment applied to 2018 |

27a. |

00 |

b. |

2018 estimated payments |

27b. |

00 |

c. |

2018 extension payment |

27c. |

00 |

d. |

For amended returns |

27d. |

00 |

e. |

For amended returns |

00 |

|

f. |

Add lines 27a through 27d, then subtract line 27e. This is your total return payments |

27f. |

|

28. Add lines 22 and 23, then subtract lines 26 and 27f. This is your amount due or (overpaid) |

28. |

||

Penalties and Interest (see instructions) |

|

|

|

29 a. Partnership information return late filing penalty |

29a. |

00 |

|

b. Interest on underpayment of estimated composite tax |

29b. |

00 |

|

c. Composite income tax return late filing penalty |

29c. |

00 |

|

d. Late payment penalty |

29d. |

00 |

|

e. Interest |

29e. |

00 |

|

f. |

Add lines 29a through 29e. This is your total penalties and interest |

29f. |

|

Amount Owed or Refund |

|

|

|

30. Add lines 28 and 29f |

30. |

||

31. If line 30 results in an amount due, enter it here. This is the amount you owe |

31. |

||

00

00

00

00

00

00

Pay online at revenue.mt.gov. If writing a check, make it payable to MONTANA DEPARTMENT OF REVENUE.

32.If line 30 results in an overpayment, enter it here. This is your overpayment. Enter as a positive number. 32.

33.Enter the amount from line 32 that you want applied to your 2019 composite

.............................................................................................estimated tax |

33. |

|

00 |

|

34. Subtract line 33 from line 32 and enter the amount here. This is your refund |

................................. |

34. |

||

00

00

00

00

Direct Deposit |

1. RTN# |

|

|

|

|

|

|

|

|

|

2. ACCT# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Your Refund |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Complete 1, 2, 3 and 4 |

3. |

If using direct deposit, you are required to mark one box. ► |

|

|

Checking |

|

|

Savings |

|

|

|

|

|

|

|

|

||||||||||||||||||||

(see instructions). |

4. |

Is this refund going to an account that is located outside of the |

United States or its territories? |

|

|

Yes |

|

No |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of false swearing, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.

Signature of Officer |

Date |

Printed Name and Title |

|

Telephone Number |

||||||||||||||||||||

|

X ____________________________________________ |

|

M |

M |

D |

D |

Y |

Y |

Y |

Y |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print/Type Preparer’s Name

Firm’s Name

Preparer’s SignatureDate

____________________________________ |

M M D D Y Y Y Y |

Firm’s Address |

Telephone Number |

PTIN

Firm’s FEIN |

May the DOR discuss this tax return with your tax preparer?  Yes

Yes

No

No

*18DY0201*

*18DY0201*

Form

Schedule I - Apportionment Factors for Multistate Partnerships

Enter amounts in columns A and B. Enter percentages in column C. |

A. Everywhere |

B. Montana. |

C. Factor |

1.Property Factor: Use average value for real and tangible personal property.

1a. |

.............................................................................................Land |

|

|

00 |

|

|

|

|

|

00 |

|

|

1b. |

......................................................................................Buildings |

|

|

00 |

|

|

|

|

|

00 |

|

|

....................................................................................1c. Machinery |

|

|

00 |

|

|

|

|

|

00 |

|

||

1d. |

Equipment |

1d. |

|

|

00 |

|

|

|

|

|

00 |

|

1e. |

...................................................................Furniture and fixtures |

|

|

00 |

|

|

|

|

|

00 |

|

|

1f. |

.........................................................Leases and leased property |

|

|

00 |

|

|

|

|

|

00 |

|

|

1g. |

...................................................................................Inventories |

|

|

00 |

|

|

|

|

|

00 |

|

|

1h. |

........................................................................Depletable assets |

|

|

00 |

|

|

|

|

|

00 |

|

|

1i. |

........................................................................Supplies and other |

|

|

00 |

|

|

|

|

|

00 |

|

|

..................1j. Property of foreign subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

||

....1k. Property of unconsolidated subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

||

1l. |

.....Property of |

|

|

00 |

|

|

|

|

|

00 |

|

|

............................1m.Multiply amount of rents by 8 and enter result |

1m. |

|

|

00 |

|

|

|

|

|

00 |

|

|

....................................Total Property Value add lines 1a through 1m |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your |

property |

factor |

1. |

|

|

|

|||||

2. Payroll Factor: |

|

|

|

|

|

|

|

|

|

|

|

|

2a. |

.............................................................Compensation of officers |

|

|

00 |

|

|

|

|

|

00 |

|

|

2b. |

.....................................................................Salaries and wages |

|

|

00 |

|

|

|

|

|

00 |

|

|

|

Payroll included in: |

|

|

|

|

|

|

|

|

|

|

|

2c. |

.....................................................................Costs of goods sold |

|

|

00 |

|

|

|

|

|

00 |

|

|

2d. |

..................................................Other expenses and deductions |

|

|

00 |

|

|

|

|

|

00 |

|

|

2e. |

....................Payroll of foreign subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

2f. |

........Payroll of unconsolidated subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

2g. |

......Payroll of |

|

|

00 |

|

|

|

|

|

00 |

|

|

........................................Total Payroll Value add lines 2a through 2g |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your payroll |

|

factor |

2. |

|

|

|

|||||

3. Gross Receipts Factor: |

|

|

|

|

|

|

|

|

|

|

|

|

3a. |

.............................Gross Receipts, less returns and allowances |

3a. |

|

|

00 |

|

|

|

|

|

|

|

3b. |

Receipts delivered or shipped to Montana purchasers: |

|

|

|

|

|

|

|

|

|

|

|

|

.................................................................................(1) Shipped from outside Montana |

|

3b.(1) |

|

|

00 |

|

|||||

|

...................................................................................(2) Shipped from within Montana |

|

3b.(2) |

|

|

00 |

|

|||||

3c. Receipts shipped from Montana to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

........................................................................................(1) United States government |

|

3c.(1) |

|

|

|

|

00 |

|

|||

|

..........................................(2) Purchasers in a state where the taxpayer is not taxable |

|

|

|

|

00 |

|

|||||

3d. |

......................Receipts other than receipts of tangible personal property (e.g. service income) |

3d. |

|

|

|

|

00 |

|

||||

3e. |

........Net gains reported on federal Schedule D and Form 4797 |

3e. |

|

|

00 |

|

|

|

|

|

00 |

|

3f. |

....................Other gross receipts (rents, royalties, interest, etc.) |

|

|

00 |

|

|

|

00 |

|

|||

3g. |

................Receipts of foreign subs included in combined group |

3g. |

|

|

00 |

|

|

|

00 |

|

||

3h. |

...Receipts of unconsolidated subs included in combined group |

3h. |

|

|

00 |

|

|

|

00 |

|

||

3i. Receipts |

|

|

|

|

|

|

|

|

|

|

|

|

|

. ................................................included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

3j. |

............................................Less: All intercompany transactions |

|

|

00 |

|

|

|

|

|

00 |

|

|

......................................Total Receipts Value add lines 3a through 3j |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your receipts |

factor |

3. |

|

|

|

|

|||||

.................................................4. Add the percentages on lines 1, 2, and 3 in column C. This is the sum of your factors |

|

|

|

4. |

|

|

|

|

||||

5.Divide the percentage on line 4 by the number of factors included in the calculation of line 4. If a property,payroll

or receipts factor is 0%, it is included in the calculation of line 4 if there’s is a value in column A (see instructions). |

|

Enter the result here and also on page 1, line 19 of this form. This is your apportionment factor |

5. |

%

%

%

%

%

*18DY0301*

*18DY0301*

Form

|

Schedule II - Montana Partnership Tax Credits |

|

|

Type of Credit |

Amount of Credit |

|

|

1. |

Dependent Care Assistance Credit |

|

|

|

|

|

|

|

|

|

include Form DCAC |

||||

2. |

College Contribution Credit |

|

|

|

|

|

|

|

|

|

|

include Form CC |

|||

3. |

Health Insurance for Uninsured Montanans Credit |

|

|

|

|

|

|

|

|

|

|

include Form HI |

|||

4. |

Recycle Credit |

|

|

|

|

|

|

|

|

|

include Form RCYL |

||||

5. |

Alternative Energy Production Credit |

|

|

|

|

|

|

|

|

|

include Form AEPC |

||||

6. |

Contractor’s Gross Receipts Tax Credit. If multiple CGR accounts, mark here. |

||||||||||||||

|

CGR Account ID: |

|

|

|

|

|

|

|

|

|

|

C |

G |

R |

|

7. |

.......................................................................................................Alternative Fuel Credit |

|

|

|

|

|

|

|

|

|

|

|

include Form AFCR |

||

8. |

Infrastructure User Fee Credit |

|

|

|

|

|

|

|

|

|

include Form IUFC |

||||

9. |

Historic Property Preservation Credit |

|

|

|

|

|

|

|

include federal Form 3468 |

||||||

10. |

Mineral and Coal Exploration Incentive Credit |

|

include Forms |

||||||||||||

11. |

Empowerment Zone Credit |

|

|

|

|

|

|

|

|

|

|

|

|

||

12. |

Biodiesel Blending and Storage Credit |

|

|

|

|

|

|

|

|

|

include Form BBSC |

||||

13.Innovative Educational Program Credit.............................................................................................................

14.Student Scholarship Organization Credit ..........................................................................................................

15. Emergency Lodging Credit |

include Form ELC |

16.Unlocking Public Lands Credit...........................................................................................................................

17.Apprenticeship Tax Credit..................................................................................................................................

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Type of Credit Recapture |

Amount of Credit |

|

|

|

Recapture |

18. |

Historic Property Preservation Credit Recapture |

00 |

19. |

Film Production Credit Recapture |

00 |

20. |

Biodiesel Blending and Storage Credit Recapture |

00 |

21. |

Oilseed Crushing and Biodiesel/Biolubricant Production Credit Recapture |

00 |

When attributing any credit or credit recapture from a partnership to its partners, use the same proportion the partnership used to report each partner’s income or loss for Montana tax purposes. Include a detailed breakdown that shows each partner’s share of the credit or credit recapture.

Use Montana Schedule

*18DY0401*

*18DY0401*

Form |

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

Schedule IV – Montana Partnership Composite Income Tax Schedule |

|

|

|

|

|

|

|

|

|

||

Part I. Eligible Participating Partners

Enter the number of eligible participating partners. See instructions for more information about eligible participating partners.

Part II. Composite Tax Ratio |

1 |

|

2 |

3 |

|

Use the amount in column 3 |

Enter the amount from |

Enter the amount from |

|

Divide column 2 by |

|

to complete the calculation |

page 1, line 15 |

page 1, line 21 |

|

column 1 |

|

|

Do not enter more than |

||||

in column H below. |

of this form. |

of this form. |

|

1.000000 |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Part III. Enter below in columns A through H the required information and amounts for each eligible participating partner. |

|

|

|

|

|||||||||||

|

|

A |

B |

C |

D |

E |

F |

G |

H |

||||||

|

|

|

Social security |

|

|

|

|

|

|

Montana taxable |

|

|

Montana composite |

||

|

|

|

number or |

Partner’s share of |

|

|

|

|

Enter the appropriate |

income tax. Multiply |

|||||

|

|

Name |

Standard |

Exemption |

income – Subtract |

||||||||||

|

|

federal employer |

federal income from |

deduction |

$2,440 |

columns D and E |

tax from the tax table |

column G times |

|||||||

|

|

|

identification |

entity |

below. |

composite tax ratio |

|||||||||

|

|

|

|

|

|

|

from column C. |

||||||||

|

|

|

number |

|

|

|

|

|

|

|

|

from Part II. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

1. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

2. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

3. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

4. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

5. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

6. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

7. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

8. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

9. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

10. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

11. |

|

Enter the total composite tax from all additional |

pages, if used |

|

|

|

|

|

|

|

|

|

11. |

|

00 |

|

|

|

|

Add column H, lines 1 through 11. This is your total composite income tax liability. |

|

00 |

|||||||||

|

|

|

Transfer the amounts from column H to each partner’s Montana Schedule |

|

|

||||||||||

*18DY0501*

*18DY0501*

If additional space is needed, make copies of this page. Include all additional pages from line 11 with the tax return.

If Your Taxable |

But Not More Than |

Multiply Your |

And Subtract |

This Is Your |

|

|

Income Is More Than |

Taxable Income By |

Tax |

|

|

||

|

|

|

|

|

|

|

$0 |

$3,000 |

1% (0.010) |

$0 |

|

|

|

$3,000 |

$5,200 |

2% (0.020) |

$30 |

|

|

|

$5,200 |

$8,000 |

3% (0.030) |

$82 |

|

|

|

$8,000 |

$10,800 |

4% (0.040) |

$162 |

|

|

|

$10,800 |

$13,900 |

5% (0.050) |

$270 |

|

|

|

$13,900 |

$17,900 |

6% (0.060) |

$409 |

|

|

|

|

More Than $17,900 |

6.9% (0.069) |

$570 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

Schedule VI – Reporting of Special Transactions

Complete Schedule VI only if your partnership filed any of the federal income tax forms described below. Mark the appropriate box indicating which form(s) you filed with the Internal Revenue Service for this tax year. If your answer is “Yes” to one or more of these forms, you need to include a complete copy of your federal tax return Form 1065.

|

1. |

The partnership filed federal Form 8918 – Material Advisor Disclosure Statement with the Internal |

|

|

|

|

Revenue Service. |

Yes |

|

|

|

Material advisors to any reportable transactions must file Form 8918. |

|

|

|

2. |

The partnership filed federal Form 8824 – |

Yes |

|

|

|

NOTE: Mark the box if your |

||

|

|

|

|

|

|

|

have to report a |

|

|

|

|

Use Form 8824 to report each exchange of business or investment property for property of a like- |

|

|

|

|

kind. |

|

|

|

3. |

The partnership filed federal Form 8865 – Return of U.S. Persons With Respect to Certain |

|

|

|

|

Foreign Partnerships with the Internal Revenue Service. |

Yes |

|

|

|

Use Form 8865 to report the information required under 26 USC 6038 (reporting with respect to |

|

|

|

|

controlled foreign partnerships), Section 6038B (reporting of transfers to foreign partnerships) or |

|

|

|

|

Section 6046A (reporting of acquisitions, dispositions and changes in foreign partnership interest). |

|

|

|

4. |

The partnership filed federal Form 8886 – Reportable Transaction Disclosure Statement with the |

|

|

|

|

Internal Revenue Service. |

Yes |

|

|

|

Use Form 8886 to disclose information for each reportable transaction in which you participated. |

|

|

Complete this section if you made a disbursement to a related party.

5.During this tax year, the partnership made payments to one or more related parties

(excluding salary compensation) that exceed $100,000 per recipient.

If you answer “Yes” to this question, please provide the name and federal employer identification number of each related party below and the amount that you paid to each related party:

Name |

|

|

|

|

FEIN |

Amount of Payment |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes

*18DY0601*

*18DY0601*

| Fact | Description |

|---|---|

| E-filing Requirement | Partnerships with more than 100 partners must file Form PR-1 electronically. |

| Inclusion of Federal Forms | A complete copy of federal Form 1065 along with all related forms and schedules must be included with the submission. |

| Type of Returns | Form PR-1 accommodates Initial, Final, Amended, and Refund returns. |

| Partners' Information | The form requires detailed information on resident and nonresident partners, including the number of Schedules K-1 included. |

| Governing Law | Form PR-1 is governed by Montana state tax laws and regulations. |

| Composite Tax and Withholding | The form calculates Montana total composite tax and summarizes withholding requirements and payments attributable to the partnership. |

Filling out the Montana PR-1 form is a critical process for partnerships operating within the state, especially when considering the detailed information and specific calculations required. The form caters to partnerships with more than 100 partners, mandating e-filing, and requires an extensive breakdown of income, deductions, and tax credits among other financial details. Successful completion involves careful preparation, including having federal tax information at hand, notably the federal Form 1065 and related schedules. Here’s a step-by-step guide to navigate the process.

After these steps are completed and the form is thoroughly reviewed, submit it either electronically, as required for partnerships with more than 100 partners, or mail it to the appropriate address if applicable. Ensuring all details are correct and documentation is complete will facilitate a smoother processing of the form.

Form PR-1, known as the Montana Partnership Information and Composite Tax Return, is used by partnerships to report their income, deductions, and taxes owed to the state of Montana. It also serves to allocate income between resident and nonresident partners and calculate the composite tax owed by the partnership on behalf of its eligible partners.

Yes, partnerships with more than 100 partners are required to e-file the PR-1 form. This ensures efficient processing and management of tax returns by the Montana Department of Revenue.

Partnerships must include a complete copy of the federal Form 1065 and all related forms and schedules when filing the Montana PR-1. This comprehensive documentation helps cross-verify the financial information provided to the state with that reported to the federal government.

While the form provided here is for the calendar year 2018 or the tax year beginning in 2018, Form PR-1 is updated annually to reflect the current tax year. When preparing to file, partnerships should ensure they are using the correct version of the form for the specific tax year they are reporting.

Form PR-1 allows for the classification of the tax return as an initial return, final return, amended return, or refund return. This distinction helps the Montana Department of Revenue understand the nature of the submission and process it accordingly.

Income and deductions are reported in two sections: Partners’ Distributive Share of Income Items and Partners’ Distributive Share of Deduction Items. These sections help break down the various categories of income and deductions similar to federal Form 1065, Schedule K, allowing partners to understand their distributive shares.

Montana additions and deductions to income on Form PR-1 allow for adjustments specific to Montana tax laws, such as interest and dividends not taxable under the Internal Revenue Code or interest on U.S. government obligations. These adjustments ensure that the income is accurately reflected according to state tax regulations.

These schedules are used to determine the portion of the partnership's income that is attributable to Montana. Apportionment factors like property, payroll, and gross receipts help calculate Montana source income by determining the extent of the partnership's business involvement within the state.

Tax credits are reported on Schedule II of Form PR-1, listing specific types of credits available to the partnership and its partners. This includes credits for dependent care assistance, college contributions, and alternative energy production, among others, enabling partnerships to reduce their overall tax liability.

The composite tax is calculated using Schedule IV, which combines eligible participating partners' Montana taxable income to compute a composite tax ratio and resulting tax owed. This simplifies tax reporting for partnerships by allowing them to pay on behalf of eligible partners, ensuring compliance with state tax obligations.

When filling out the Montana PR-1 form, people commonly make a number of mistakes. It's essential to avoid these errors to ensure the form is processed correctly and efficiently. Here are five such mistakes:

Not e-filing when required: Partnerships with more than 100 partners must e-file the Montana PR-1 form. Failing to do so can result in penalties and processing delays.

Incomplete federal documentation: A common oversight is not including a complete copy of the federal Form 1065, along with all related forms and schedules. This is crucial as it provides a detailed picture of the partnership’s financial activities.

Miscalculation of income: Accurately calculating the partners’ distributive share of income items can be complex. Mistakes often occur in the transfer of figures from federal forms or in the addition and subtraction within the income sections of the form.

Incorrect number of Schedules K-1 included: Every partner should have a Schedule K-1, and failing to include the correct number of these schedules can lead to processing issues and may potentially affect the accuracy of reported income and deductions.

Errors in apportionment calculation: For partnerships operating in multiple states, calculating the correct apportionment factor for Montana source income is vital. Errors in the property, payroll, and gross receipts factors can lead to inaccurate state income allocation.

Avoiding these mistakes requires a thorough review process and a clear understanding of the form's requirements. Here are additional tips for ensuring accuracy:

Double-check all entries for mathematical accuracy.

Ensure all necessary documentation is attached before filing.

Review the instructions for each section carefully to ensure compliance with specific requirements.

Consult with a tax professional if there are uncertainties or complex partnership activities that might affect the filing.

Use the direct deposit option for refunds to avoid delays in receiving payments.

By paying close attention to these details, partnerships can avoid common pitfalls and ensure their Montana PR-1 form is filled out accurately and completely.

When managing partnerships or handling tax matters in Montana, especially with the Montana Form PR-1, several other forms and documents might be essential for completion and submission to ensure compliance and accuracy during the filing process. Understanding the scope and requirement of each can streamline your tax preparation efforts and ensure that all relevant information is accurately reported to the Montana Department of Revenue. Below is a brief overview of forms and documents often used alongside the Montana PR-1 form.

Each of these documents plays a crucial role in ensuring that the partnership’s tax obligations are met accurately and comprehensively. The specific requirements may vary depending on the partnership’s activities during the fiscal year, as well as any credits or deductions for which the partnership is eligible. Proper organization and understanding of these forms can significantly ease the filing process, ensuring compliance with both federal and state tax laws.

The Montana PR-1 form is reminiscent of the federal Form 1065, U.S. Return of Partnership Income. Both forms are used by partnerships to report income, financial operations, and distributions to partners. The Montana PR-1 requires a complete copy of the federal Form 1065, underscoring their intertwined nature. Each form collects detailed financial information, including income or loss from operations, deductions, and partner distributions, ensuring both federal and state tax obligations are met based on the partnership's operations.

Similar to Schedule K-1 (Form 1065), which is issued by partnerships to report each partner's share of the partnership's earnings, deductions, and credits to the IRS, the Montana PR-1 form also requires details about the distributive share of income to partners. It necessitates the inclusion of Schedules K-1 in the filing process, showcasing the allocation of income, gains, losses, deductions, and credits to the partners. Both documents are essential for partners to accurately report their portion of partnership income or loss on their personal tax returns.

The Montana PR-1 form echoes elements found in the Schedule IV – Montana Partnership Composite Income Tax Schedule, a specific component of the state's partnership filing requirements. This resemblance is due to its aim to calculate and report composite income tax for eligible partners, a process akin to consolidating tax payments or obligations for partners at the state level. This schedule facilitates a streamlined tax payment process for partnerships and their partners, similar to the PR-1’s overall objective of gathering and reporting partnership financial activities for state tax purposes.

Furthermore, the form parallels the information requested by Form 4797, Sales of Business Property, which is required for federal tax purposes. Both documents deal with the disposition of property and the associated gains or losses. The PR-1 requests details of net section 1231 gains or losses, which includes transactions reported on Form 4797, emphasizing the taxation of partnership property transactions both federally and at the state level in Montana.

Another document that shares similarities with the Montana PR-1 form is the federal Form 8825, Rental Real Estate Income and Expenses of a Partnership or an S Corporation. Both require detailed reporting of income and expenses from rental real estate operations. The PR-1 form specifically asks for net rental real estate income or loss, including amounts from Form 8825, ensuring that partnerships accurately report their real estate operations' financial impact at both the state and federal levels.

The form also aligns with the federal Form 4562, Depreciation and Amortization. Through its requirement for reporting section 179 deductions, the Montana PR-1 necessitates that partnerships detail their capital expenditures and depreciation claims, similarly to how Form 4562 is used to calculate and report depreciation for federal tax purposes. This connection underscores the tax implications of partnership investments in business assets, aligning state and federal tax reporting practices.

Last, the similarities extend to the Schedule I - Apportionment Factors for Multistate Partnerships, akin to various state and federal schedules aiming to allocate income and operations across jurisdictions. The PR-1 form's inclusion of apportionment and allocation schedules reflects the broader tax principle of determining tax obligations based on the geographical source of income. These elements are critical for partnerships operating in multiple states, ensuring taxes are accurately levied according to the origin of income and the presence of operations within Montana versus other states.

When entering information into the Montana PR-1 form, attention to detail and adherence to specific guidelines are crucial for a smooth process. Below are outlined steps on what you should and shouldn't do to help you navigate the form accurately.

Do:Misconceptions about the Montana Form PR-1, which covers Partnership Information and Composite Tax Return, are common among partnerships and tax preparers. Clarifying these misconceptions is essential for accurate and compliant tax filing.

Fact: Partnerships with more than 100 partners are mandated to e-file, indicating that not all partnerships have the flexibility to choose their filing method.

Fact: This form is also relevant for partnerships operating in Montana but formed in other states, as it requires information on the state of formation.

Fact: A comprehensive copy of the federal Form 1065 and all related forms and schedules must be included, requiring detailed financial information.

Fact: The form encompasses various return types including initial, final, amended, and refund returns, suggesting the need for historical as well as current year data.

Fact: Detailed sections on partners’ distributive share of income and deductions indicate these figures are vital for accurate calculation of Montana income and deductions.

Fact: The form requires information on both Montana additions to income and Montana deductions, showing that various non-taxable income and expense categories must be reported and can affect the tax outcome.

Fact: The form incorporates sections for both partnership tax credits and payments made by the partnership, requiring a detailed enumeration of credits and payments, including specific forms and schedules related to different types of credits.

Fact: The form specifies that for using direct deposit, certain conditions must be met, including marking the type of account and stating whether the refund is going to an account outside the United States or its territories.

Dispelling these misconceptions ensures that partnerships engaging in business within Montana can file their tax returns accurately and in compliance with state requirements, avoiding potential penalties for incorrect or incomplete information.

When dealing with the Montana PR-1 form for partnership information and composite tax return purposes, it is crucial to be aware of several key aspects to ensure accuracy and compliance. Here are five important takeaways:

This brief overview emphasizes the importance of paying close attention to the details and requirements of the Montana PR-1 form to ensure proper compliance and to take full advantage of the tax benefits available to partnerships operating within the state.

Can a Homeowner Replace an Electrical Outlet - Unlock the potential of your new construction projects with this Electrical Permit Application, tailored for both residential and commercial ventures in Missoula County.

Montana 283 - Designed to guide petitioners through the legal process of requesting an update to a parenting plan, ensuring all requisite information and documentation is systematically presented.