Fillable Montana Apls101F Template in PDF

Fillable Montana Apls101F Template in PDF

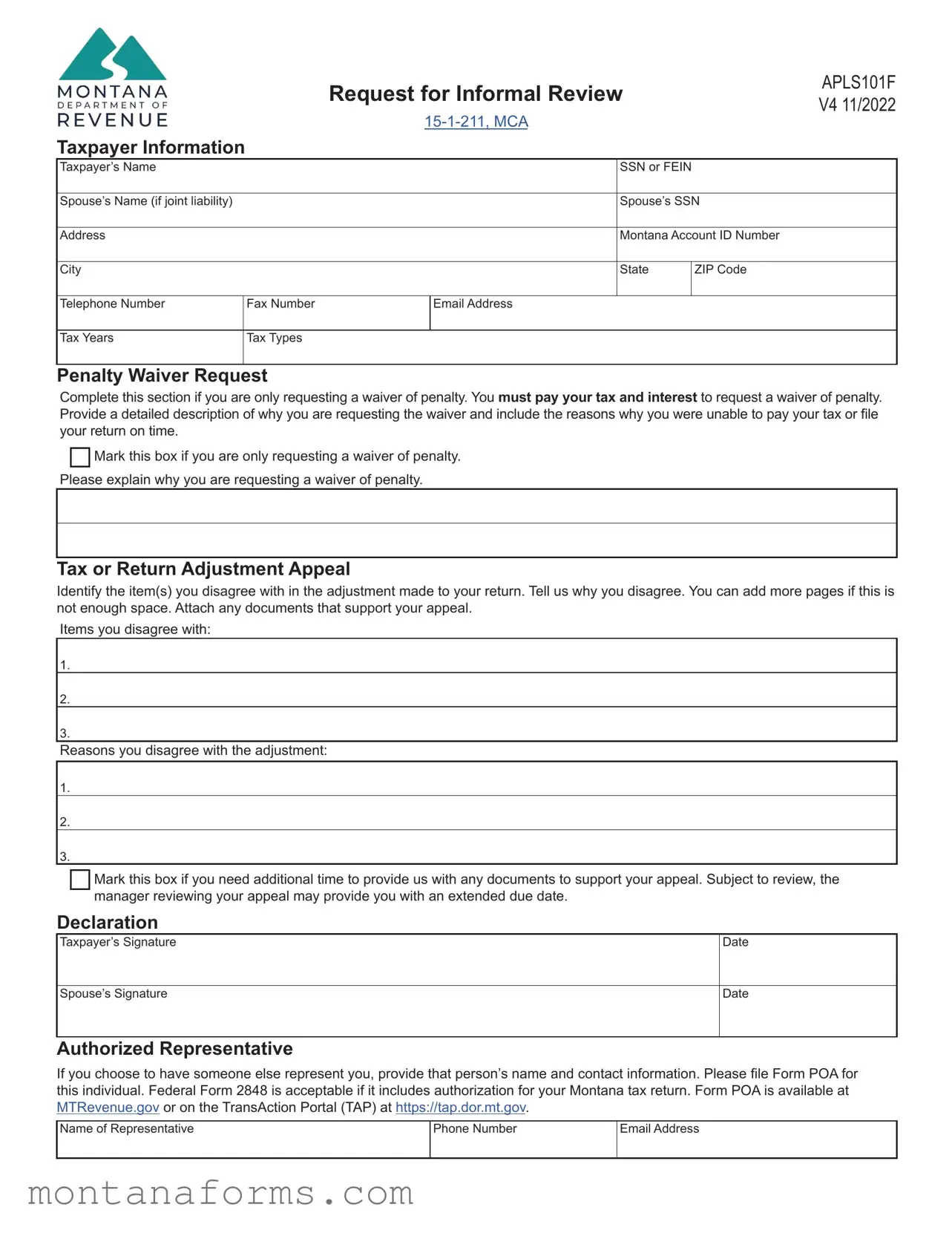

The Montana APLS101F form serves as a vital tool for taxpayers seeking to navigate the complexities of adjusting their tax returns or appealing penalties. This form is specifically designed for those who have received a Notice of Assessment (NOA) and believe there has been an error in the adjustment of their tax return, or for individuals seeking a waiver for penalties imposed due to late tax payments or filings. Upon receiving an NOA, which could be an audit determination letter, a return adjustment notice, or a first bill indicating a change in the owed amount or a reduction in the refund, taxpayers have a 30-day window to submit this form to request an informal review. This process is integral for voicing disagreements with the adjustments made, offering a platform to provide detailed reasons and supporting documents to contest the department's decision. For cases involving penalties, the form allows taxpayers to present circumstances that prevented timely payment or filing, potentially leading to a waiver if deemed to have sufficient cause. The appeal process outlined requires prompt action, underscoring the importance of adhering to deadlines to ensure the taxpayer's right to contest adjustments or penalties is preserved. Submitted via email, mail, or fax, this form not only initiates a review by a department manager but also provides an opportunity for further recourse through the Office of Dispute Resolution if the initial appeal does not resolve the issue to the taxpayer's satisfaction. The Montana Department of Revenue offers this form and accompanying guidance as a means to ensure fairness and accuracy in tax assessment and enforcement, welcoming inquiries and providing necessary assistance through various communication channels.

|

|

|

Request for Informal Review |

APLS101F |

||

|

|

|

V4 11/2022 |

|||

|

|

|

|

|

|

|

|

|

|

|

|||

Taxpayer Information |

|

|

|

|

|

|

Taxpayer’s Name |

|

|

|

SSN or FEIN |

|

|

|

|

|

|

|

|

|

Spouse’s Name (if joint liability) |

|

|

|

Spouse’s SSN |

||

|

|

|

|

|

|

|

Address |

|

|

|

Montana Account ID Number |

||

|

|

|

|

|

|

|

City |

|

|

|

State |

ZIP Code |

|

|

|

|

|

|

|

|

Telephone Number |

|

Fax Number |

|

Email Address |

|

|

|

|

|

|

|

|

|

Tax Years |

|

Tax Types |

|

|

|

|

|

|

|

|

|

|

|

Penalty Waiver Request

Complete this section if you are only requesting a waiver of penalty. You must pay your tax and interest to request a waiver of penalty.

Provide a detailed description of why you are requesting the waiver and include the reasons why you were unable to pay your tax or file your return on time.

Mark this box if you are only requesting a waiver of penalty.

Please explain why you are requesting a waiver of penalty.

Tax or Return Adjustment Appeal

Identify the item(s) you disagree with in the adjustment made to your return. Tell us why you disagree. You can add more pages if this is not enough space. Attach any documents that support your appeal.

Items you disagree with:

1.

2.

3.

Reasons you disagree with the adjustment:

1.

2.

3.

Mark this box if you need additional time to provide us with any documents to support your appeal. Subject to review, the manager reviewing your appeal may provide you with an extended due date.

Declaration

Taxpayer’s Signature

Spouse’s Signature

Date

Date

Authorized Representative

If you choose to have someone else represent you, provide that person’s name and contact information. Please file Form POA for this individual. Federal Form 2848 is acceptable if it includes authorization for your Montana tax return. Form POA is available at

MTRevenue.gov or on the TransAction Portal (TAP) at https://tap.dor.mt.gov.

Name of Representative

Phone Number

Email Address

Request for Informal Review Instructions

Purpose of this form

You may use this form to request an informal review of a

Notice of Assessment (NOA) or to request a waiver of penalty. An NOA is the first notice that the department will send you

if we adjust your return, change the amount you owe, or reduce your refund. It may come to you in the form of an audit determination letter, a return adjustment notice, or as

your first bill. An informal review is a written request to have a

department manager review the determination outlined in your

NOA. If you disagree with the NOA, use this form to begin

the informal review process. You must submit a request for informal review within 45 days of the date on your NOA.

A Statement of Account (SOA) is a bill that you will receive

if you do not request an informal review or pay the balance due showing on your NOA. You will continue to receive an SOA on a monthly basis until you pay the amount on the bill. If you disagree with a balance on an SOA, you may use this

form to tell us why you were unable to ask for an informal

review of the NOA you previously received. If we determine

that your failure to respond within 45 days was due to

reasonable cause, we will then evaluate your concerns over the NOA you received. Reasonable cause means that you

exercised ordinary business care but were still unable to meet a department deadline.

We will also accept a separate written request for an informal review of your NOA or SOA. You may mail, email,

or fax your request for informal review to the contact information in your notice or these instructions.

Penalty waiver

We automatically waive your late payment penalty if you

pay your tax and interest within 30 days of the date on your NOA. If you were unable to pay your tax and interest within 30 days of the date on the NOA due to unforeseen

circumstances, you can use this form to request a waiver of penalty if you believe you have reasonable cause. You must pay tax and interest before we can consider waiving any penalties.

Once we receive your request, an auditor will review it to

determine if you qualify for a waiver. We will send you a letter informing you of our decision within 30 days of your

request. If we deny your request for a waiver of penalty, you may request an informal review of our denial by filing

this form within 45 days of the date on our denial letter.

Appeal process and timing

When we make an adjustment to your tax return or amount owed you have the right to request an informal review for the department to review that change.

If you disagree with the adjustment on your NOA, you

must send us a written request for an informal review

within 45 days of the date on the NOA. Your request must

explain why you disagree with our adjustment. Include any documents that support your position.

Once we receive your appeal, it will be forwarded to a

department manager to review the adjustment. The manager will review your request and the work of the auditor who made the adjustment and send you a response within 45 days that outlines whether or not we agree with your request.

If you did not send your request for informal review within

45 days of the date on the NOA, we consider it to be a

deemed admission that you agree with our adjustment. At that point, you can no longer appeal the adjustment we made unless you demonstrate that you had reasonable cause for missing the 45 day deadline. We will review the

reasons you provide and determine if there is reasonable cause to review the adjustment. Once our review is

complete, we will send you a response with our decision.

If we determine that you had reasonable cause to miss your appeal deadline, you can file an informal review of the

adjustment we made to your return.

Our response will inform you if we agree or disagree with your appeal. It will also explain our reasons for disagreement so that you understand our decision. If you disagree with our decision, you may request further review by sending Form APLS102F,

Notice of Referral to the Office of Dispute Resolution, to the Office of Dispute Resolution within 45 days from the notice of determination date. The Office of Dispute Resolution is an

independent division within the department which may hear

taxpayer appeals at the request of the taxpayer. They can either act as a mediator or issue a final department decision.

Form APLS102F is available at MTRevenue.gov.

Filing this form

Email this form and supporting documents to

DORObjections@mt.gov. Mail to:

Montana Department of Revenue

DOR Objections

P.O. Box 7149

Helena, MT

Administrative Rules of Montana: 42.2.510, 42.2.512

Questions? Call us at (406)

| Fact | Detail |

|---|---|

| Form Number | APLS101F |

| Version | V3 8/2021 |

| Purpose | Request for Informal Review of a Notice of Assessment (NOA) or Request for Penalty Waiver |

| Governing Law | Montana Code Annotated (MCA) 15-1-211 |

| Submission Deadline | Within 30 days of the date on your NOA |

| Penalty Waiver Criteria | Must pay tax and interest within 30 days of NOA date to request a penalty waiver |

| Appeal Process Timing | Manager will review and respond to appeal within 30 days of receipt |

| Administrative Rules of Montana References | 42.2.510, 42.2.512 |

| Contact Information for Filing | Email: DORObjections@mt.gov, Mail: Montana Department of Revenue, DOR Objections, P.O. Box 7149, Helena, MT 59604-7149 |

| Additional Information | To appoint a representative, file Form POA or Federal Form 2848 if it includes authorization for Montana tax return |

Facing an adjustment on your tax return or needing a penalty waiver can be daunting. Fortunately, the Montana APLS101F form is designed to streamline the process of requesting an informal review of a Notice of Assessment (NOA) or applying for a penalty waiver. This process is critical to ensure that any disputes or misunderstandings with tax assessments are clarified and resolved with the Montana Department of Revenue. Following the correct steps to fill out this form is imperative to ensure that your request is processed efficiently.

After filling out the form, review all sections carefully to ensure accuracy and completeness. Then, according to your preference or convenience, email the form along with any supporting documents to DORObjections@mt.gov or mail it to the Montana Department of Revenue at the address provided. Timeliness is crucial, so ensure your request for an informal review or penalty waiver is submitted within 30 days of receiving your NOA. This step is the beginning of the appeal process, and adhering to the guidelines will facilitate a smoother review of your case, potentially leading to a favorable resolution.

What is the purpose of the Montana APLS101F form?

The Montana APLS101F form is designed for taxpayers to request an informal review of a Notice of Assessment (NOA) or to appeal a penalty waiver. An NOA is a notification from the Montana Department of Revenue indicating an adjustment to your tax return, a change in the amount you owe, or a revision of your refund. This form allows taxpayers to have a department manager reevaluate the adjustments or penalties applied. It's an opportunity to explain your position, submit additional documentation, and potentially reverse or amend the decision. The ultimate goal is to ensure fair and accurate tax assessments and penalties.

How can someone request a penalty waiver using the APLS101F form?

To request a penalty waiver, you must complete the specific section for penalty waiver requests on the APLS101F form. This involves paying the tax and interest due and providing a detailed explanation of why you were unable to pay or file your tax return on time. It is necessary to demonstrate unforeseen circumstances or reasonable cause for failing to meet the tax obligations within the stipulated timeframe. Once filled, you must mark the designated box on the form to indicate you are requesting a penalty waiver exclusively.

What is the appeal process and timeline when using the APLS101F form?

Upon disagreeing with an adjustment made to your tax return, you need to submit a written appeal using the APLS101F form within 30 days from the date on your NOA. Your appeal should delineate why you disagree with the adjustment and include any supporting documents. After submission, your appeal will be reviewed by a department manager, who will then provide a response within 30 days. If you fail to appeal within this 30-day period, it's considered a tacit agreement with the adjustment. However, if you missed the deadline due to reasonable cause, you may still file an appeal, provided you can substantiate the cause. If the appeal is granted, the department will review the adjustment again and communicate their final decision. For disagreements with the final decision, further review can be requested by sending Form APLS102F to the Office of Dispute Resolution within 30 days.

How should the APLS101F form be submitted?

The APLS101F form, along with any supporting documentation, can be submitted via email or mail. To submit via email, send it to DORObjections@mt.gov. If preferring mail, the form should be sent to the Montana Department of Revenue at DOR Objections, P.O. Box 7149, Helena, MT 59604-7149. It is essential to ensure that all relevant sections of the form are completed and that any supporting documents are included to facilitate a thorough review of your request or appeal.

Not providing complete taxpayer information, including the Taxpayer’s Name, SSN or FEIN, and Montana Account ID Number, can lead to processing delays. It's essential to fill in every field to ensure that the request is associated with the correct account.

Omitting the spouse’s details, such as the Spouse’s Name and SSN, in cases of joint liability, might result in an incomplete review of the case, as all parties involved must be correctly identified.

Failure to thoroughly explain the reason behind a penalty waiver request. A detailed description, including why the taxpayer was unable to pay their tax or file the return on time, is crucial for the waiver to be considered.

Forgetting to mark the box indicating a request for a penalty waiver. This misstep can lead to unnecessary delays because it might not be immediately clear what the taxpayer is requesting.

Not identifying the specific items of disagreement in the Tax or Return Adjustment Appeal section leaves the review incomplete. It is imperative that taxpayers clearly articulate the points of contention and why they disagree with the adjustment made to their return.

Skimping on attaching supporting documents for the appeal. These documents are vital for substantiating the appeal. Failing to attach them can weaken the case, hindering the ability to have the appeal favorably reviewed.

Filing beyond the 30-day deadline: Waiting more than 30 days from the date on the Notice of Assessment (NOA) to submit a request for informal review or to appeal an adjustment can be an irreversible mistake. It's considered a deemed admission of agreement with the adjustment, limiting the right to appeal unless reasonable cause is demonstrated.

Ignoring the option for extended document submission times: Not marking the box to request additional time for providing supporting documents can result in a missed opportunity. This request is crucial if the initial appeal does not include all necessary evidence but could be strengthened with additional documents.

Neglecting to utilize the TransAction Portal (TAP): Many overlook the ease and efficiency of submitting their forms and documents through the TAP, an online tool available for such purposes. This platform often streamlines the submission process, making it simpler to lodge an appeal or request.

Incorrect contact information: A common, yet critical mistake is providing outdated or incorrect phone numbers and email addresses. This error can result in missed communication about the appeal, potentially leading to an unfavorable outcome due to unresponsiveness.

When dealing with tax matters in Montana, particularly pertaining to the Montana APLS101F form, several other forms and documents might be relevant for a comprehensive approach to handling one's tax affairs. These documents play crucial roles in different contexts, from appointing a representative to appealing department decisions or resolving disputes. Understanding these forms can help ensure that you navigate the tax landscape more effectively.

Each of these documents plays a distinct role in the tax management process, providing pathways for representation, appeal, and resolution. Taxpayers should familiarize themselves with these forms to navigate tax proceedings confidently or seek professional advice to ensure proper handling of their tax obligations in Montana.

The IRS Form 1040X, "Amended U.S. Individual Income Tax Return," is similar to the Montana APLS101F form in its purpose of correcting previously filed tax returns. Both forms allow taxpayers to amend inaccuracies or claim refunds that were not previously claimed. The 1040X form, like the APLS101F form, requires detailed explanations for the adjustments being requested, along with documentation to support these amendments.

The IRS Form 843, "Claim for Refund and Request for Abatement," has similarities to the Montana APLS101F in terms of seeking relief from penalties. Both forms provide a platform for taxpayers to request a waiver of penalties due to reasonable cause, such as unforeseen circumstances that prevented timely payment. Taxpayers must provide a detailed explanation and, if applicable, documentation to support their claim for both forms.

The IRS Form 656, "Offer in Compromise," although different in its primary purpose of settling tax debts for less than the amount owed, shares a similarity with the APLS101F’s aspect of requesting consideration due to special circumstances. Both forms require the taxpayer to provide detailed information about their financial situation and reasons for the request, thereby requiring thorough evaluation by the respective tax authority.

State-specific tax appeal forms, similar to the one used in Montana (APLS101F), are common across various states, allowing taxpayers to contest assessments or penalties. These forms generally require the taxpayer to identify the specific issues in dispute, provide evidence supporting their position, and explain why the original assessment was incorrect, mirroring the process described in the APLS101F.

The IRS Form 8857, "Request for Innocent Spouse Relief," while focusing specifically on requesting relief from joint tax liabilities, shares a commonality with Montana’s APLS101F form in the appeal process. Both forms invite taxpayers to present their case, providing explanations and attaching necessary documentation to support their relief or appeal requests.

The California FTB Form 2917, "Request for Innocent Joint Filer Relief," is similar to Montana's form in that it provides taxpayers a means to appeal tax liabilities or penalties based on special circumstances, such as being unaware of errors caused by the other spouse. Both forms emphasize the importance of detailed explanations supported by documentary evidence.

The New York State Form IT-280, "Nonresident Group Return," allows representatives of groups of taxpayers to contest tax issues, a feature that is somewhat mirrored in the representation aspect of the APLS101F form. In Montana’s form, taxpayers can designate an authorized representative, much like the group return allows for a collective appeal process.

The Texas Comptroller’s "Request for Redetermination" form is used to contest tax or penalty assessments made by the state, similar to the purpose of Montana's APLS101F form. Taxpayers must provide reasons and evidence to support their disagreement with the assessment, which closely aligns with the appeal process described in the APLS101F form.

The Georgia Department of Revenue's "Petition for Reassessment" allows taxpayers to appeal against tax decisions, paralleling the APLS101F form's function. Both forms serve as a medium for taxpayers to argue against adjustments made by the tax authority, requiring a detailed explanation of the dispute and submission of any relevant supporting documents.

The Pennsylvania Department of Revenue "Petition for Refund" form, similar to the Montana APLS101F, offers taxpayers a pathway to dispute taxes, penalties, or interest assessed by the state. Both forms necessitate a clear delineation of the issue, a logical explanation for the appeal, and submission of any pertinent evidence to back the taxpayer's claims.

Understanding the importance and complexity of filing forms like the Montana APLS101F is crucial for ensuring your request for an informal review or a penalty waiver is considered adequately by the Montana Department of Revenue. Here's a concise guide to assist you in this process:

Do These:

Don't Do These:

Filling out the Montana APLS101F form correctly and thoughtfully can significantly influence the outcome of your request. Paying attention to the details and following these dos and don'ts will facilitate a smoother process in handling your tax matters with the Montana Department of Revenue.

When dealing with tax forms like the Montana APLS101F, it's easy for taxpayers to be overwhelmed or misunderstanding certain aspects of the process. Here are eight common misconceptions about this form and what you really need to know:

It's only for disputing tax amounts. While it's true that the APLS101F form is often used to request an informal review of a Notice of Assessment or a tax return adjustment, it’s also used for requesting a penalty waiver. This means if there are valid reasons like unforeseen circumstances that prevented timely tax or interest payment, taxpayers can appeal against penalties.

Requesting a waiver of penalty requires immediate full payment of taxes and interest. While taxpayers are encouraged to pay their tax and interest when requesting a penalty waiver to qualify, it’s crucial to understand that the form includes sections to explain reasons for the waiver request. This provides an opportunity to present a case even if full payment has not been made yet.

An informal review can be requested anytime. The APLS101F must be submitted within 30 days of the Notice of Assessment date. This deadline is crucial for a taxpayer wanting to appeal the department’s decision. Waiting too long might lead to a deemed admission, where the taxpayer agrees with the adjustment by default.

All appeals require extensive documentation. While supporting documents are essential for substantiating an appeal, the form allows taxpayers to mark a box if they need additional time to gather documentation. This flexibility helps ensure that the appeal process is not hindered by the immediate availability of supporting documents.

The decision after an informal review is final. After an informal review, if the taxpayer disagrees with the department's decision, further action can be taken by filing Form APLS102F for a review by the Office of Dispute Resolution. This means there are additional steps available for those unsatisfied with the outcome of their informal review.

Any communication method is acceptable for submitting the form. While it might seem convenient to use any communication means, the APLS101F form should be submitted through the specific channels provided by the Montana Department of Revenue. These include email, traditional mail, or fax, ensuring the appeal is formally recorded and processed.

The form serves no purpose if the deadline is missed. Even if the 30-day deadline for an informal review request following a Notice of Assessment is missed, the taxpayer might still have a recourse. If there is a reasonable cause for the delay, explained in a separate written request, the department may consider the appeal.

Filing this form is complex and requires legal assistance. Although legal or tax professional advice can be invaluable, the form is designed to be user-friendly. Clear instructions and designated sections for each type of appeal make it feasible for taxpayers to proceed without immediate professional assistance, especially for straightforward cases.

Understanding these misconceptions can help navigate the review process more effectively, reduce anxiety about the appeal procedure, and ensure that rights and opportunities for a fair hearing are well-utilized.

Filling out and using the Montana APLS101F form is a crucial process for taxpayers seeking an informal review of a Notice of Assessment (NOA) or a penalty waiver. Understanding the correct way to use this form is important for effectively communicating with the Montana Department of Revenue. Here are key takeaways to guide you through this process:

Can a Homeowner Replace an Electrical Outlet - Transform your living space safely with this application, covering all your bases from new construction to minor electrical upgrades.

What Wages Are Subject to Illinois Unemployment Tax - Identification of owners or corporate officers is required, with space for additional attachments if needed.

Montana Income Tax Forms - Taxpayers can designate a third party to discuss their return with tax authorities via the 2EZ form, reflecting flexibility in managing their tax affairs.