Fillable Montana 2Ez Template in PDF

Fillable Montana 2Ez Template in PDF

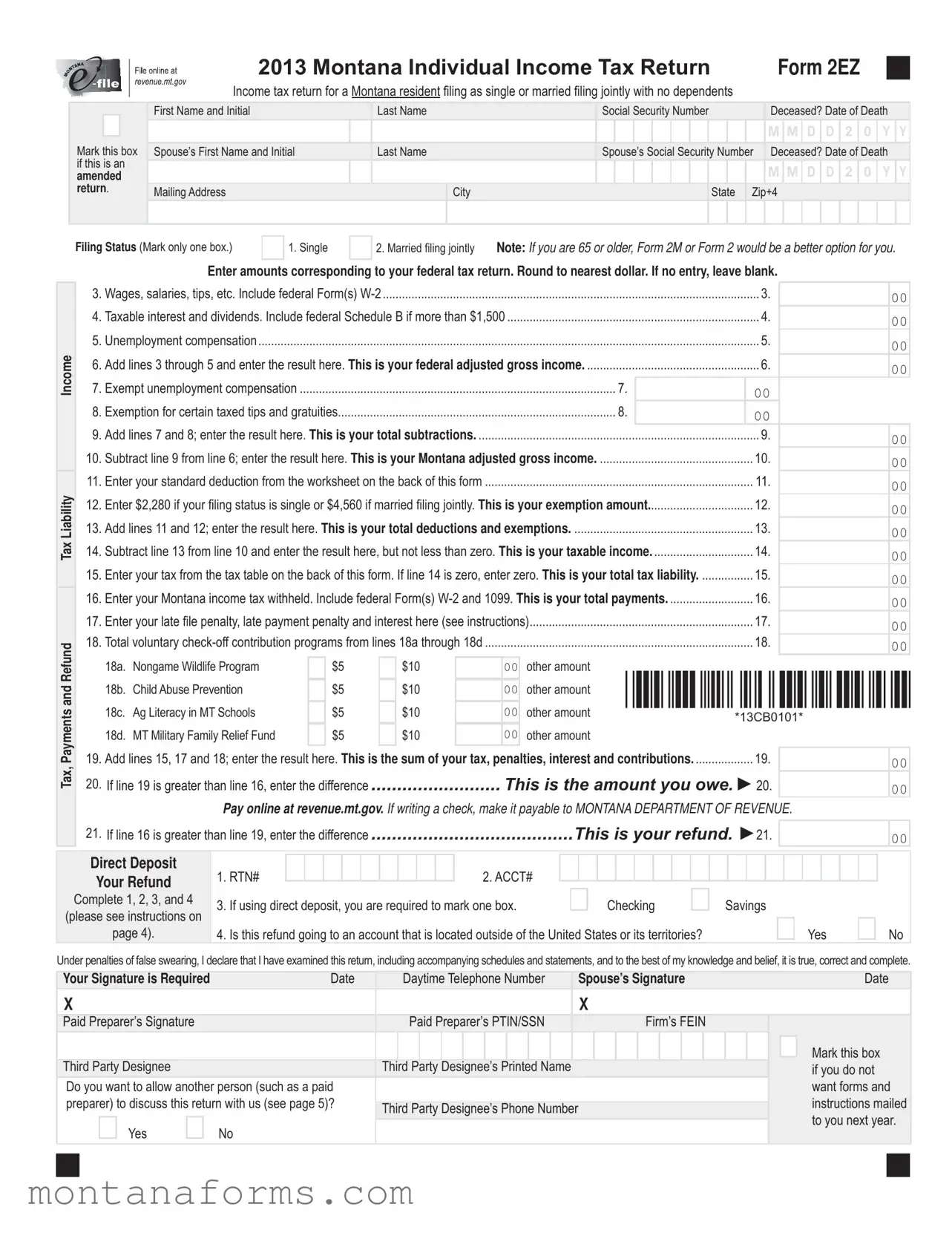

Filing income tax returns is an essential duty for residents across the United States, and Montana is no exception. The Montana 2EZ form serves as a simplified method for individuals residing in Montana to file their annual income tax returns. Designed for either single individuals or married couples filing jointly without dependents, it streamlines the filing process. This form is particularly tailored for those whose financial situations do not warrant the complexities found in other forms. Key information required on the form includes wages, salaries, tips, taxable interest, dividends, and unemployment compensation. Taxpayers must calculate their federal adjusted gross income, make allowable subtractions, and then determine their Montana adjusted gross income to find out their tax liability. Additionally, the form covers exemptions, deductions, and calculates the total tax liability, offering a section for direct deposit of any refunds. Taxpayers also have the opportunity to contribute to voluntary check-off programs benefiting various causes. It’s important to note that there are specific conditions under which Montanans can file this simplified form, including provisions for those who are 65 or older or have special financial situations, suggesting that the 2EZ form may not be suitable for everyone. Whether filing an original or amended return, the 2EZ form integrates aspects of standard deduction and provides worksheets to aid in accuracy, ensuring that the taxpayers meet their obligations with ease.

2013 Montana Individual Income Tax Return |

Form 2EZ |

|

Income tax return for a Montana resident filing as single or married filing jointly with no dependents

Mark this box if this is an amended

return.

First Name and Initial |

Last Name |

Social Security Number |

Deceased? Date of Death |

|

|

|

|

|

|

|

|

|

|

|

|

M |

M |

D |

D |

2 |

0 |

Y |

Y |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s First Name and Initial |

Last Name |

Spouse’s Social Security Number Deceased? Date of Death |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

M |

M |

D |

D |

2 |

0 |

Y |

Y |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

City |

|

|

|

|

|

|

State |

Zip+4 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Filing Status (Mark only one box.)

1. Single

2.Married filing jointly Note: If you are 65 or older, Form 2M or Form 2 would be a better option for you.

Enter amounts corresponding to your federal tax return. Round to nearest dollar. If no entry, leave blank.

|

3. |

Wages, salaries, tips, etc. Include federal Form(s) |

|

|

|

|

|

|

3. |

|

00 |

|

|||||||

|

4. |

Taxable interest and dividends. Include federal Schedule B if more than $1,500 |

|

|

4. |

|

|

|

|||||||||||

|

|

|

|

00 |

|

||||||||||||||

|

5. |

Unemployment compensation |

|

|

|

|

|

|

|

|

|

|

5. |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income |

6. |

.Add lines 3 through 5 and enter the result here. This is your federal adjusted gross income |

|

6. |

|

00 |

|

||||||||||||

7. |

...................................................................................................Exempt unemployment compensation |

|

|

|

|

|

|

|

|

7. |

|

|

00 |

|

|

|

|||

|

8. |

Exemption for certain taxed tips and gratuities....................................................................................... 8. |

|

|

00 |

|

|

|

|||||||||||

|

9. |

Add lines 7 and 8; enter the result here. This is your total subtractions. |

........................................................................................ |

|

|

|

|

9. |

|

00 |

|

||||||||

|

10. |

Subtract line 9 from line 6; enter the result here. This is your Montana adjusted gross income |

|

10. |

|

|

|

||||||||||||

|

|

|

00 |

|

|||||||||||||||

|

11. |

Enter your standard deduction from the worksheet on the back of this form |

|

|

11. |

|

|

|

|||||||||||

|

|

|

|

00 |

|

||||||||||||||

Liability |

13. |

Add lines 11 and 12; enter the result here. This is your total deductions and exemptions |

|

13. |

|

|

|

||||||||||||

|

|

00 |

|

||||||||||||||||

|

12. |

Enter $2,280 if your filing status is single or $4,560 if married filing jointly. |

This is your exemption amount |

12. |

|

00 |

|

||||||||||||

Tax |

14. |

Subtract line 13 from line 10 and enter the result here, but not less than zero. This is your taxable income |

14. |

|

|

|

|||||||||||||

|

00 |

|

|||||||||||||||||

|

15. |

Enter your tax from the tax table on the back of this form. If line 14 is zero, enter zero. This is your total tax liability |

15. |

|

|

|

|||||||||||||

|

|

00 |

|

||||||||||||||||

|

16. |

Enter your Montana income tax withheld. Include federal Form(s) |

16. |

|

|

|

|||||||||||||

|

|

00 |

|

||||||||||||||||

|

17. |

Enter your late file penalty, late payment penalty and interest here (see instructions) |

|

17. |

|

|

|

||||||||||||

|

|

|

00 |

|

|||||||||||||||

Refundand |

18. |

Total voluntary |

|

|

18. |

|

|

|

|||||||||||

|

|

|

00 |

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

18b. |

Child Abuse Prevention |

|

|

$5 |

|

$10 |

|

|

|

other amount |

*13CB0101* |

|||||||

|

|

|

|

|

|

00 |

|||||||||||||

|

|

18a. |

Nongame Wildlife Program |

|

|

$5 |

|

$10 |

|

|

00 |

other amount |

|

|

|

|

|

|

|

Payments |

|

18c. Ag Literacy in MT Schools |

|

|

$5 |

|

$10 |

|

|

|

other amount |

|

|

|

|

|

|

|

|

19. |

|

|

the |

|

|

00 |

|

.................. |

19. |

|

00 |

|

|||||||

Add lines 15, 17 and 18; enter the result |

|

here. This is |

sum of your tax, |

penalties, interest and contributions. |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*13CB0101* |

|

|

||

|

|

18d. MT Military Family Relief Fund |

|

|

$5 |

|

$10 |

|

|

00 other amount |

|

|

|

|

|

|

|

||

Tax, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20. If line 19 is greater than line 16, enter the difference |

|

|

|

This is the amount you owe. ►20. |

|

|

|

||||||||||||

|

|

|

00 |

|

|||||||||||||||

Pay online at revenue.mt.gov. If writing a check, make it payable to MONTANA DEPARTMENT OF REVENUE.

|

21. If line 16 is greater than line 19, enter the difference |

|

|

|

|

|

|

This is your refund. ►21. |

|

|

|

|

|

|

|

|

00 |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct Deposit |

1. RTN# |

|

|

|

|

|

|

|

|

|

2. ACCT# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your Refund |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete 1, 2, 3, and 4 |

3. |

If using direct deposit, you are required to mark one box. |

|

|

|

|

Checking |

|

Savings |

|

||||||||||||||||||||||||||

(please see instructions on |

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

page 4). |

4. |

Is this refund going to an account that is located outside of the United States or its territories? |

|

|

|

|

|

|

|

Yes |

|

|

No |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of false swearing, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct and complete.

Your Signature is Required |

Date |

Daytime Telephone Number |

Spouse’s Signature |

Date |

X |

|

|

|

|

|

|

|

|

|

|

X |

|

||||||||||||||||

Paid Preparer’s Signature |

|

|

Paid Preparer’s PTIN/SSN |

|

|

|

Firm’s FEIN |

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mark this box |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Third Party Designee |

|

Third Party Designee’s Printed Name |

|

|

|

|

|

|

|

|

|

|

|

if you do not |

|

|||||||||||||

Do you want to allow another person (such as a paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

want forms and |

|

||||||

preparer) to discuss this return with us (see page 5)? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

instructions mailed |

|

||||||

Third Party Designee’s Phone Number |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to you next year. |

|

||||||||||

|

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

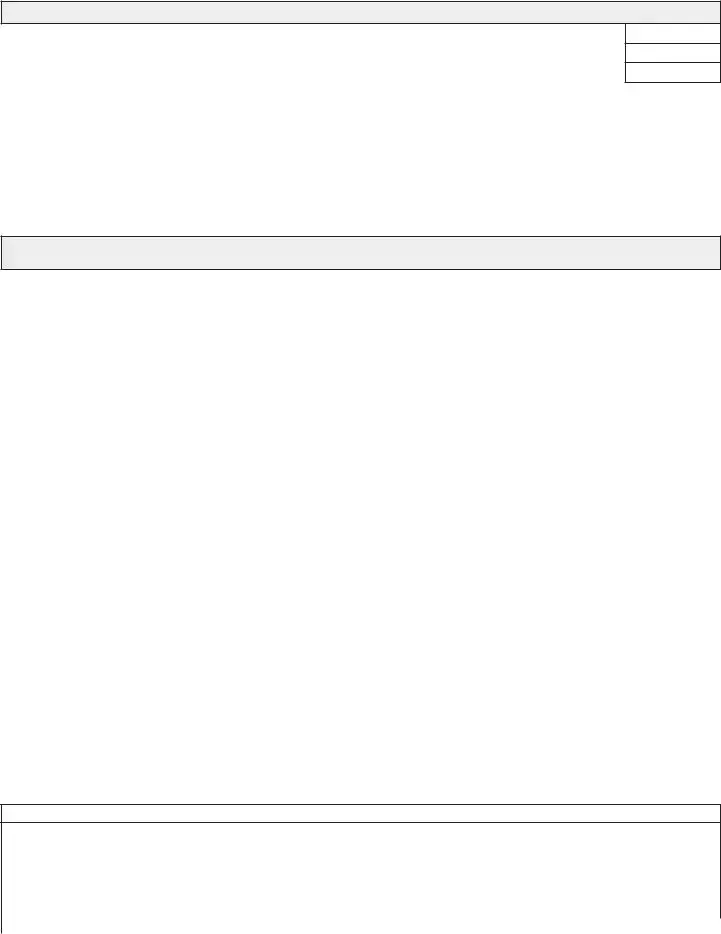

Form 2EZ - Worksheets and Tax Table

Standard Deduction Worksheet

1. |

Enter your Montana adjusted gross income from Form 2EZ, line 10 here |

1. |

|

2. |

Multiply the amount on line 1 by 20% (0.20) and enter the result here |

2. |

|

3. |

Enter the amount below that corresponds to your filing status here |

3. |

|

|

• If your filing status is single (filing status 1), enter $4,270. This is your maximum standard deduction. |

|

|

|

• If your filing status is joint (filing status 2), enter $8,540. This is your maximum standard deduction. |

|

|

4. |

Enter the amount from line 2 or 3, whichever is smaller |

4. |

|

|

|||

5. |

Enter the amount below that corresponds to your filing status |

5. |

|

|

|||

|

• If your filing status is single (filing status 1), enter $1,900. This is your minimum standard deduction. |

|

|

|

|

|

|

|

• If your filing status is joint (filing status 2), enter $3,800. This is your minimum standard deduction. |

|

|

6. |

Enter here and on Form 2EZ, line 11, the amount from line 4 or line 5, whichever is larger. This is your standard deduction |

6. |

|

|

|||

|

|

|

|

Calculation of Interest on Underpayment of Estimated Taxes – Short Method Worksheet (If you made estimated tax payments, Form 2M or Form 2 would be a better option for you.)

Montana law requires you to pay your income tax liability throughout the year. You can make your payments through employer withholding, through installment payments of estimated taxes, or through a combination of employer withholding and estimated tax payments. You are not required to make estimated tax payments if one of the following conditions applies to you:

•Your combined tax liability after you applied your withholding and estimated tax payments is less than $500.

•You did not have a 2012 income tax liability and you were a citizen or resident of the United States the entire year.

•You retired in either 2012 or 2013 after reaching the age of 62.

•You became disabled in either 2012 or 2013.

•You are a farmer or rancher and

If you did not pay in advance at least 90% of your 2013 income tax liability (after applying your credits) or 100% of your 2012 income tax liability (after applying your credits), you may have to pay interest on the underpayment of your estimated taxes.

If you are required to pay interest on your underpayment, you can use this short method to determine your interest, but only if one of the following conditions applies to you:

•You made no estimated tax payments (in other words, your only payments were Montana withholding); or

•You made four equal estimated payments by the required due dates.

If you are not eligible to use this short method to calculate your interest on your underpayment, use Montana Form

1. |

Enter here your 2013 total tax liability as reported on Form 2EZ, line 15 |

1. |

|

2. |

Multiply line 1 by 90% (0.90) and enter the result here |

2. |

|

|

|||

3. |

Enter the amount from Form 2EZ, line 16 here |

3. |

|

|

|||

4. |

Subtract line 3 from line 1 and enter the result here. If your result is $500 or less, stop here; you do not owe interest on your |

|

|

|

|

||

|

underpayment |

4. |

|

5. |

Enter here the 2012 income tax liability that you reported on your 2012 Form 2, line 54; Form 2M, line 47; or Form 2EZ, line 15 |

5. |

|

|

|||

6. |

Enter the smaller of line 2 or line 5 here |

6. |

|

|

|||

7. |

Enter the amount from Form 2EZ, line 16 here |

7. |

|

|

|||

8. |

Subtract line 7 from line 6 and enter the result here. If the result is zero or less, stop here; you do not owe interest on your |

|

|

|

|

||

|

underpayment. This is your total underpayment for 2013 |

8. |

|

9. |

Multiply line 8 by 0.05320 and enter the result here |

9. |

|

|

|||

10. |

If you paid the amount on line 8 before April 15, multiply the amount on line 8 by the number of days you paid before April 15, and |

|

|

|

|

||

|

then multiply by 0.0002192 |

10. |

|

11. |

Subtract line 10 from line 9 and enter the result here and on Form 2EZ, line 17. This is your interest on underpayment of |

|

|

|

|

||

|

estimated taxes |

11. |

|

|

|

|

|

2013 Montana Individual Income Tax Table

If Your Taxable |

But Not |

Multiply |

And |

This Is |

Income Is |

More Than |

Your Taxable |

Subtract |

Your Tax |

More Than |

Income By |

|||

$0 |

$2,800 |

1% (0.010) |

$0 |

|

$2,800 |

$4,900 |

2% (0.020) |

$28 |

|

$4,900 |

$7,400 |

3% (0.030) |

$77 |

|

$7,400 |

$10,100 |

4% (0.040) |

$151 |

|

If Your Taxable |

But Not |

Multiply |

And |

This Is |

Income Is |

More Than |

Your Taxable |

Subtract |

Your Tax |

More Than |

Income By |

|||

$10,100 |

$13,000 |

5% (0.050) |

$252 |

|

$13,000 |

$16,700 |

6% (0.060) |

$382 |

|

More Than $16,700 |

6.9% (0.069) |

$532 |

|

|

For example: |

Taxable income $6,800 X 3% (0.030) = $204. |

$204 minus $77 = $127 tax |

| Fact | Detail |

|---|---|

| Form Purpose | The Montana 2EZ form is used for filing an individual income tax return for residents who are single or married filing jointly without dependents. |

| Filing Status Options | Eligible filers can mark their status as either single or married filing jointly on the form. |

| Eligibility for Seniors | If a filer is 65 years or older, the form recommends using Form 2M or Form 2 for potential tax benefits. |

| Adjustment and Deduction | The form allows adjustments for certain types of income and claims standard deductions before computing the tax liability. |

| Governing Law | The form is governed by Montana state law, specifically pertaining to the administration of state income tax within Montana. |

Filling out your Montana 2EZ tax form doesn't have to be a daunting task. It's designed for Montana residents who are either single or married filing jointly, without dependents. This straightforward guide will walk you through each step, ensuring that your tax return is completed accurately and on time. Whether this is your first time filing taxes or you just need a quick refresher, these instructions will simplify the process.

After completing these steps, double-check your form for accuracy to ensure all information is correct and no steps have been missed. This careful review can help prevent delays in processing your tax return. Once satisfied with your review, you can submit your completed form to the Montana Department of Revenue by the due date to avoid any late filing penalties. Remember, the information provided here is designed to guide you through the form's completion process, offering clarity and support along the way.

What is the Montana 2EZ form?

The Montana 2EZ form is a simplified state income tax return designed for Montana residents who are either single or married and filing jointly without any dependents. Suitable for those with straightforward tax situations, it includes sections for reporting wages, salaries, tips, taxable interest, dividends, and unemployment compensation.

Who should use the Montana 2EZ form?

If you're a Montana resident filing as single or married filing jointly, and you do not have any dependents, the Montana 2EZ form might be right for you. However, if you are 65 or older, you might benefit from filing Form 2M or Form 2 instead. The simplicity of the 2EZ form is ideal for those with uncomplicated tax situations who want a straightforward way to file their taxes.

Can I file the Montana 2EZ form if I have earned interest or dividends?

Yes, you can file the Montana 2EZ form if you have earned interest or dividends. However, if your total taxable interest and dividends exceed $1,500, you must include Federal Schedule B with your return. This form accommodates reporting for typical sources of income, including wages, interest, and dividends, as long as they fall within the specified guidelines.

What are the tax benefits of filing a Montana 2EZ form?

Filing the Montana 2EZ form offers the benefit of simplicity and speed in tax preparation and filing, especially for those with straightforward financial situations. By using this form, you can quickly calculate your Montana adjusted gross income, standard deduction, and total tax liability. It guides you through a few short steps to determine your taxable income and total tax, as well as any refund or amount owed.

How do I calculate my standard deduction on the Montana 2EZ form?

To calculate your standard deduction on the Montana 2EZ form, you first determine your Montana adjusted gross income and then apply the specified percentages to find the appropriate deduction amount. The form offers a worksheet on the back to help you calculate this. Your filing status significantly influences your standard deduction, with different base amounts and caps for single and joint filers. This calculation ensures that you claim the optimal standard deduction for your situation, impacting your taxable income and overall tax liability.

Not marking the appropriate filing status. For individuals in Montana using the 2EZ form, the selection between "single" or "married filing jointly" is crucial. This decision impacts the calculation of taxes owed or refunds due. A mistake in this section leads to inaccuracies in the tax liability or benefit.

Entering incorrect Social Security numbers. A common error involves inaccurately inputting either the taxpayer's or spouse's Social Security Number. This misstep can cause delays in processing or result in the mismatching of earnings records, affecting tax calculations and identity verification processes.

Failure to include taxable interest and dividends. Taxpayers often overlook or improperly report income from interest and dividends, especially if it exceeds $1,500, which necessitates the inclusion of a federal Schedule B. Neglecting this detail may lead to underreported income and potential penalties.

Omitting federal adjusted gross income figures. The form requires that amounts corresponding to federal tax returns be entered, specifically for wages, salaries, tips, etc. Erroneously leaving this blank or providing inaccurate figures can affect the calculation of Montana adjusted gross income, leading to incorrect tax outcomes.

Incorrectly calculating the standard deduction. The standard deduction amount is pivotal in determining taxable income. It varies based on income and filing status. Taxpayers often err in this calculation by not following the worksheet on the back of the form meticulously, thereby inflating or deflating their taxable income inaccurately.

Excluding total payments or incorrectly reporting Montana income tax withheld. This includes not only the withholding from form(s) W-2 and 1099 but also estimated tax payments, if applicable. Such omissions or inaccuracies can result in miscalculated refunds or amounts owed, along with possible penalties for underpayment.

Failing to accurately report or calculate interest on underpayments of estimated taxes when required. This situation typically arises when taxpayers are oblivious of their obligation to make estimated tax payments, or when they misunderstand the calculation method provided by the short method worksheet. Overlooking this detail can lead to unplanned interest charges.

Not utilizing direct deposit options for refunds correctly. By mismanaging the direct deposit information, including routing and account numbers or failing to indicate the account type correctly, taxpayers risk delays in receiving refunds or misrouting of funds.

Omission of voluntary check-off contributions. While not directly impacting the tax calculation, neglecting the opportunity to contribute to programs like Child Abuse Prevention or Nongame Wildlife Program through the tax return can mean missing a chance to support vital state initiatives.

Inaccuracies in signatures and dates. The absence of required signatures and dates invalidates a tax return, necessitating its resubmission. This mistake can delay the processing of returns and subsequent refunds.

When filing the Montana 2EZ form, which is the 2013 Montana Individual Income Tax Return Form for residents filing as single or married filing jointly with no dependents, individuals often need to gather additional documents and forms to ensure their tax return is accurate and complete. These documents can provide essential information related to income, deductions, and any tax credits to which the filer might be entitled. Below is an outline of other forms and documents frequently used alongside the Montana 2EZ form.

Collecting and organizing these documents before starting the tax filing process can streamline the preparation of the Montana 2EZ form, ensure accuracy, and potentially maximize your refund or minimize your tax liability. It's important to review each document's requirements and how they relate to your individual tax situation.

The 1040EZ federal income tax return form is closely related to the Montana 2EZ form. Both forms are designed for simplicity, catering to individuals or married couples with no dependents, offering a straightforward tax filing experience. While the 1040EZ form serves taxpayers across the United States, the Montana 2EZ specifically caters to Montana residents, reflecting the state's tax codes and regulations.

The 540 2EZ form used by the State of California is another comparable document to Montana's 2EZ form. Like Montana's version, California's 2EZ form is intended for residents with uncomplicated financial situations, allowing for an expedited filing process that emphasizes ease over the depth of detail. Both forms accommodate filers with specific income types and straightforward tax situations.

Form IT-201, used for New York State's resident income tax return, shares similarities with Montana's 2EZ form in its purpose to collect state tax from residents. While New York's form is more complex and caters to a broader range of tax situations, both forms serve the essential function of facilitating state income tax reporting for residents, albeit with differences in scope and applicability based on their respective state's tax laws.

The Pennsylvania Income Tax Return (PA-40) is akin to the Montana 2EZ form in that it is tailored to the state's residents, gathering income details to compute tax liability. Both forms cater to individual filing needs within their respective states, with specific lines dedicated to income, deductions, and taxes owed. The difference lies in the detailed requirements and tax treatments specific to each state's regulations.

Ohio's IT 1040 form shares a foundation with Montana's 2EZ through its role in the state tax system, providing a means for residents to report income and calculate taxes due. Designed with the taxpayer in mind, both forms streamline the process for individuals with straightforward financial situations, ensuring compliance with state tax obligations.

The Colorado Individual Income Tax Form (104) parallels the Montana 2EZ form in its function as a state-level tax return document. Both are integral to their respective state tax systems, requiring income reporting for tax calculations. The focus of each form is to facilitate tax compliance in a structured yet accommodating manner for residents.

Form IL-1040, the Illinois Individual Income Tax Return, bears resemblance to Montana's 2EZ in providing a state-specific platform for tax reporting and liability computation. While each form is tailored to meet the unique regulatory and tax environment of its state, both aim to simplify the tax filing process for residents with not overly complex financial conditions.

The Michigan 1040 form is another state tax document with functionalities similar to the Montana 2EZ form. As vehicles for reporting state taxes, both documents require detailed income information, enabling individuals to comply with their tax obligations efficiently. The forms are differently structured to address the tax codes of Michigan and Montana, respectively, but their core purpose aligns closely.

Georgia's Individual Income Tax Form (500) is comparably structured to serve state residents in tax reporting and calculations, akin to Montana's 2EZ form. Both states have developed these forms to streamline the filing process, ensuring residents can report their incomes and understand their tax liabilities in a straightforward manner.

The New Jersey Resident Income Tax Return (NJ-1040) shares objectives with Montana's 2EZ form, allowing for the annual reporting of income and computation of state tax liability. Both forms are designed to cater to state-specific tax requirements, facilitating a seamless tax filing experience for residents within a framework that prioritizes clarity and usability.

Wisconsin's Form 1, the Wisconsin Income Tax form, is functionally similar to the Montana 2EZ form, as both are integral to their respective state tax collection efforts. Detailing income and tax payments, they serve as the point of interaction between the taxpayer and the state's financial requirements. Though each reflects its state's tax specifics, the overarching goal is to render the tax filing process as efficient as possible for residents.

Filling out the Montana 2EZ form, a simplified individual income tax return document for Montana residents with specific filing criteria, requires careful attention to detail. To facilitate a smooth and accurate filing process, consider the following recommendations:

When it comes to understanding state income tax requirements, it's easy to stumble upon misinformation, especially regarding specific forms like the Montana 2EZ form. Here, we'll clarify four common misconceptions that might lead to confusion.

In summary, while the Montana 2EZ form is indeed tailored towards a more straightforward financial scenario, it still encompasses a range of situations more broad than many realize. It allows for some deductions and adjustments, can be used by those 65 or older if it meets their needs, and offers modern convenience for payment methods. Understanding these aspects can help taxpayers determine the most suitable filing option for their circumstances.

The Montana 2EZ form is a simplified tax document for residents who meet certain criteria. Understanding its features and how to complete it correctly can save time and ensure compliance with state tax laws. Here are key takeaways:

Before signing the form, ensure that all information is accurate to the best of your knowledge. False declarations can lead to penalties. Electronic filing options are available for a quicker processing of your return. For payment of any tax owed, options include online payment or check payable to MONTANA DEPARTMENT OF REVENUE. Always review the latest instructions or consult a tax professional if you're unsure how to proceed.

Montana Nr 1 - Filers must attach a copy of their North Dakota tax return if claiming income on line 2 of the form to ensure compliance.

Montana Alcohol Beverage Control - Maintain regulatory compliance and streamline your gaming operation’s reporting tasks with the Montana 34 form.